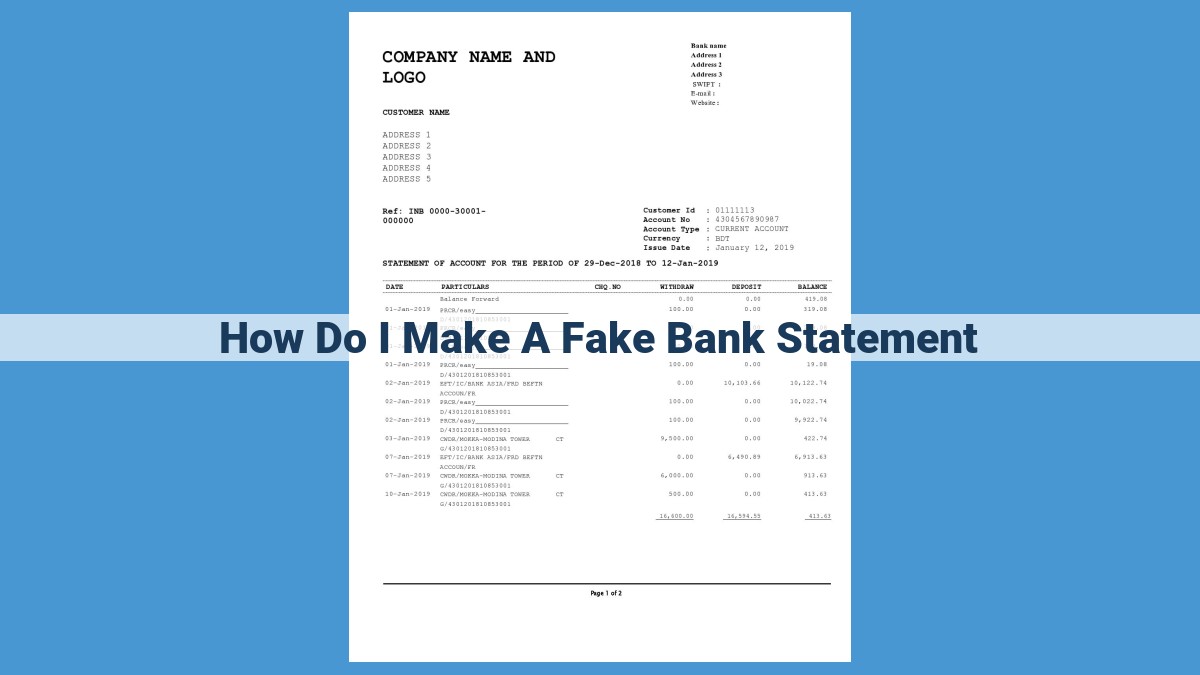

Creating fake bank statements is illegal and unethical, involving severe legal consequences and data privacy breaches. Forgery detection techniques like signature analysis and image enhancement help prevent fraud. Anti-fraud measures include customer due diligence, transaction monitoring, and security protocols. Bank reconciliation, transaction monitoring tools, and identity verification ensure account accuracy and prevent identity theft. Financial crime investigation techniques uncover fraud evidence, while document examination techniques detect forged documents, safeguarding financial institutions and individuals.

Legal and Ethical Implications

- Discuss the legal consequences of creating fake bank statements, including banking regulations, data protection laws, and fraud statutes.

- Explain the ethical considerations involved, such as maintaining confidentiality, avoiding conflicts of interest, and adhering to professional ethics.

Legal and Ethical Implications of Fabricating Bank Statements

Creating fake bank statements is a serious offense with far-reaching legal and ethical consequences.

Banking Regulations:

- Violating banking regulations by providing false information can result in penalties, fines, and even criminal charges. Banks have a legal obligation to maintain accurate and reliable records.

Data Protection Laws:

- Fabricated bank statements often involve personal financial data, which falls under the protection of data protection laws. Breaching these laws can lead to substantial penalties and reputational damage.

Fraud Statutes:

- Creating fake bank statements with the intent to deceive is a form of fraud. It can result in criminal prosecution, fines, and imprisonment.

Ethical Considerations:

Beyond the legal implications, fabricating bank statements also raises ethical concerns:

-

Maintaining Confidentiality: Accountants and financial professionals are ethically bound to maintain the confidentiality of client information. Creating fake statements undermines this trust.

-

Avoiding Conflicts of Interest: Professionals must avoid conflicts of interest. Creating fake statements for personal gain or to favor specific parties is unethical.

-

Adhering to Professional Ethics: Fabricating bank statements violates the ethical codes of professional organizations and undermines the integrity of the financial system.

Forgery Detection Methods: Unveiling the Truth in Bank Statements

In a world where financial integrity is paramount, the need for effective forgery detection methods cannot be overstated. When it comes to bank statements, a falsified document can have devastating consequences, potentially leading to fraud, identity theft, and financial ruin. To combat this threat, banks and financial institutions employ a range of techniques to scrutinize bank statements and differentiate the genuine from the fraudulent.

One such method is signature analysis. Trained professionals compare the signature on a suspect bank statement to a known, genuine signature. Discrepancies in the size, shape, slant, and pressure points of the strokes can indicate forgery.

Handwriting analysis takes this examination a step further. Examiners analyze the overall style, letter formation, and stroke patterns of the writing. Even in cases where the signature appears to match, variations in the body of the statement can reveal inconsistencies that point to forgery.

Image enhancement technologies play a vital role in detecting forged bank statements. Digital imaging techniques can reveal alterations or manipulations that may not be discernible to the naked eye. By adjusting contrast, brightness, and color balance, examiners can uncover hidden details or inconsistencies in the document’s structure.

The importance of these forgery detection methods cannot be underestimated. By using these techniques, banks and financial institutions can identify suspicious bank statements, preventing fraud and protecting the integrity of our financial system. These methods serve as a vital safeguard against those who seek to exploit vulnerabilities in our financial infrastructure.

Fraud Prevention Techniques: How Banks Keep Your Money Safe

Every day, banks work diligently to safeguard your financial well-being by implementing a robust arsenal of fraud prevention techniques. These measures, designed to identify and thwart fraudulent activities, are crucial in protecting your hard-earned money from falling into the wrong hands.

Customer Due Diligence: Knowing Your Clients

Banks play a pivotal role in combating financial crime by conducting thorough customer due diligence (CDD). This process involves verifying the identities of their clients and assessing their risk profiles. By collecting information about your personal and financial history, banks can identify potential red flags that may indicate suspicious activities.

Transaction Monitoring: Spotting Anomalies

Once your account is established, banks constantly monitor your transactions for any unusual patterns or deviations from your regular spending habits. Sophisticated algorithms and advanced analytics scan each purchase, withdrawal, and deposit, searching for signs of unauthorized activity. If anything out of the ordinary is detected, the bank will swiftly alert you.

Security Measures: Protecting Your Identity

In today’s digital age, protecting your identity is paramount. Banks employ a variety of security measures to safeguard your sensitive information, including multi-factor authentication, strong encryption, and advanced fraud detection systems. By requiring multiple forms of verification before allowing access to your account, banks make it exceptionally difficult for fraudsters to impersonate you.

Bank Reconciliation: Ensuring Accuracy in Your Financial Records

Every month, you receive a statement from your bank detailing your transactions and account balance. When you compare this statement to your own records, you’re performing a crucial process called bank reconciliation. This seemingly mundane task is vital for maintaining the accuracy and reliability of your financial records.

Bank reconciliation is not merely about matching numbers; it’s about uncovering discrepancies, detecting fraudulent activities, and ensuring the integrity of your accounts. The methods used for bank reconciliation include:

-

Account balancing: Begin by comparing your bank statement balance to your own records. If there’s a difference, you must investigate the cause.

-

Transaction matching: Go through each transaction on your bank statement and ensure it matches your records. If a transaction is missing or incorrect, investigate the error.

-

Error detection: Check for errors in calculations, such as incorrect totals or duplicate entries. These errors can lead to significant discrepancies in your financial statements.

By performing bank reconciliation regularly, you maintain a clear understanding of your financial position. It’s like having an eagle eye that spots discrepancies before they snowball into bigger problems. So, make bank reconciliation a habit to safeguard your financial well-being.

Transaction Monitoring Tools: The Digital Watchdogs of Banking Security

In today’s fast-paced digital world, banks face an ever-increasing threat of financial fraud. One of the most critical defenses against these threats is transaction monitoring tools. These sophisticated systems use advanced technologies like AI, machine learning, and rule-based systems to scan every financial transaction in real-time, searching for suspicious patterns and anomalies that may indicate fraudulent activity.

Artificial Intelligence (AI) and Machine Learning (ML) algorithms empower transaction monitoring tools with the ability to analyze vast amounts of data and identify complex patterns that would be difficult or impossible for humans to detect. These algorithms learn from historical data and adapt over time, becoming more effective at recognizing fraudulent transactions.

Rule-Based Systems complement AI and ML by defining specific rules that transactions must adhere to. These rules can be tailored to the specific risks and vulnerabilities of each bank, ensuring that unusual or suspicious transactions are flagged for further investigation.

Suspicious Patterns and Anomalies

Transaction monitoring tools search for a wide range of suspicious patterns and anomalies that may indicate fraud. These include:

- Unusual transaction amounts or frequencies

- Transactions involving known high-risk countries or individuals

- Sudden changes in spending patterns

- Multiple transactions occurring in a short period of time

Proactive Fraud Detection

By detecting these suspicious patterns, transaction monitoring tools enable banks to take proactive action against fraud. When a suspicious transaction is identified, the system can automatically block the transaction, alert the bank’s fraud team, or trigger a review process.

Enhanced Customer Protection

Transaction monitoring tools play a vital role in protecting customers from financial fraud. By identifying and blocking suspicious transactions, banks can minimize the financial losses and identity theft risks associated with fraudulent activity.

Transaction monitoring tools are indispensable in the fight against financial fraud. By harnessing the power of AI, machine learning, and rule-based systems, banks can effectively detect and prevent fraudulent transactions, ensuring the safety and security of their customers’ funds.

Account Verification Procedures: Safeguarding Your Finances

In the digital age, protecting your financial accounts from fraud is paramount. Banks employ rigorous verification procedures to ensure that account holders are who they claim to be, shielding your hard-earned money from unauthorized access.

Identity Verification: Unmasking the True Self

Banks utilize various methods to verify your identity. These may include:

- Document Verification: Checking your government-issued ID (e.g., passport, ID card) to confirm your name, photo, and signature.

- Biometric Verification: Using unique physical characteristics, such as your fingerprint, voice print, or retina scan to ascertain your identity.

- Online Verification: Conducting online identity checks through third-party service providers who verify your name, address, and other personal details.

Address Verification: Confirming Your Dwelling

Banks also verify your address to ensure it matches the one on file. This may include:

- Postal Verification: Sending a letter or postcard to your registered address for confirmation.

- Physical Verification: Sending a representative to your address to verify its existence and obtain proof of occupancy.

- Database Cross-Checking: Comparing your address against public records or utility bills to confirm its accuracy.

Phone Number Verification: Connecting the Lines

Finally, banks may verify your phone number to establish an additional layer of security. This involves:

- SMS Verification: Sending a text message with a verification code to your registered phone number.

- Call Verification: Making a phone call to your registered number and asking you to confirm your identity.

Importance of Account Verification Procedures

These verification procedures are crucial for preventing fraud. Impersonators attempting to open accounts or access funds with stolen credentials are thwarted by these measures. Furthermore, they protect banks from liability by ensuring that account holders are legitimate and have consented to any transactions.

By implementing these thorough account verification procedures, banks create a secure environment where customers can trust that their financial assets are safeguarded.

Identity Theft Prevention Measures: Empowering Banks to Safeguard Your Financial Identity

Identity theft is a growing concern in the digital age, posing significant risks to individuals and financial institutions alike. To combat this threat, banks have implemented a range of robust measures to protect customer information and prevent fraudulent activities.

Credential Theft Prevention:

Banks deploy sophisticated systems to monitor and detect attempts to steal or compromise user credentials such as passwords and login information. By analyzing login patterns, IP addresses, and device fingerprints, these systems identify suspicious activities and block unauthorized access.

Biometric Authentication:

Leveraging advanced technology, banks offer biometric authentication methods like fingerprint scanners, facial recognition, and voice recognition. These unique identifiers provide an additional layer of security, making it virtually impossible for fraudsters to impersonate legitimate account holders.

Multi-Factor Authentication (MFA):

MFA requires users to provide multiple forms of identification when accessing their accounts. This typically involves a combination of something they know (password), something they have (phone or security token), and something they are (biometric identifier). By adding an extra layer of security, MFA significantly reduces the risk of account takeovers and unauthorized transactions.

Effectiveness of Identity Theft Prevention Measures:

The implementation of these measures has proven highly effective in safeguarding customer information and deterring identity theft. Banks are constantly innovating and enhancing their security protocols to stay ahead of evolving fraudster tactics. As a result, instances of identity theft have been significantly reduced, providing peace of mind to bank customers.

Empowering Customers to Protect Their Identity

While banks play a crucial role in preventing identity theft, customers also have a responsibility to protect their own information. By following best practices such as creating strong passwords, being vigilant about phishing scams, and monitoring their credit reports, individuals can further minimize their risk of becoming victims of identity theft.

Financial Crime Investigation Techniques: Unraveling Fraud with Precision

In the intricate world of finance, fraudsters lurk in the shadows, seeking to exploit vulnerabilities and pilfer funds. To combat these malicious actors, financial crime investigators employ a multifaceted arsenal of techniques that shed light on the darkest corners of financial deceit.

Forensic Accounting: Piercing the Veil of Deception

Forensic accountants are the sleuths of the financial world, meticulously examining financial records to uncover irregularities. They trace the flow of funds, identifying any suspicious transactions or anomalies that may hint at fraud. By scrutinizing bank statements, invoices, and other financial documents, they piece together the puzzle of financial wrongdoing.

Data Analytics: Sifting through the Digital Tsunami

In the vast sea of financial data, data analytics provides investigators with a powerful tool to detect patterns and correlations that may be invisible to the naked eye. Advanced algorithms analyze millions of transactions, flagging suspicious activities that warrant further investigation. By harnessing the power of technology, investigators can efficiently sift through mountains of data, honing in on potential red flags.

Interviews: Interrogating the Truth

Direct questioning remains a cornerstone of financial crime investigation. Skilled investigators interview witnesses, suspects, and victims, carefully extracting crucial information. They employ a range of tactics, from building rapport to applying pressure, to elicit truthful accounts of the alleged fraud. By delving into the minds of those involved, investigators gain invaluable insights into the motivations and methods of the perpetrators.

Collaborative Efforts: Uniting Forces against Fraud

Financial crime investigations rarely occur in isolation. Investigators from various disciplines, including law enforcement, regulatory agencies, and forensic accountants, often collaborate to uncover the full scope of a fraud scheme. This cross-functional approach ensures that all angles are covered and that no stone is left unturned in the pursuit of justice. By pooling their expertise, investigators increase the likelihood of bringing fraudsters to account.

The Importance of Financial Crime Investigation

The consequences of financial fraud can be devastating, not only for victims but also for the integrity of the financial system. Financial crime investigators play a vital role in protecting individuals, businesses, and the economy at large by:

- Deterrence: The threat of detection and prosecution dissuades potential fraudsters from engaging in illegal activities.

- Detection: Investigators uncover hidden fraud, bringing perpetrators to light and preventing further victimization.

- Recovery: Asset recovery efforts ensure that victims of fraud are compensated for their losses.

- Justice: By holding fraudsters accountable, investigators uphold the law and restore faith in the financial system.

Financial crime investigation is a complex and demanding field, requiring a combination of analytical skills, investigative experience, and unwavering determination. Investigators navigate the treacherous terrain of fraud, armed with a multitude of techniques and a relentless pursuit of truth and justice.

Unveiling the Secrets of Forged Documents: Document Examination Techniques

In the realm of financial fraud, forged documents serve as cunning tools to deceive banks and individuals. To safeguard against this deceptive practice, investigators employ a meticulous arsenal of techniques to scrutinize documents for any signs of tampering.

Microscopic Examination: A Forensic Magnifier

Microscopy surpasses the limits of the naked eye, magnifying documents to reveal hidden details. By isolating individual fibers, ink strokes, and erasures, forensic examiners can pinpoint alterations that escape ordinary detection. This microscopic examination uncovers the telltale traces of forgery, exposing the true nature of supposedly genuine documents.

Spectroscopy: Unraveling the Invisible

Beyond the visible spectrum, spectroscopy uncovers secrets that remain concealed to the human eye. By analyzing the absorption and emission of light at specific wavelengths, spectrometers pinpoint the chemical composition of documents. This detailed analysis can identify alterations in ink formulations, revealing concealed text or revealing erasures that have been cleverly disguised.

UV Inspection: Illuminating the Darkness

Ultraviolet inspection unveils a hidden world. When documents are exposed to ultraviolet light, certain substances fluoresce, casting a telltale glow. By studying these fluorescent patterns, examiners can detect alterations, invisible to the naked eye, that may provide irrefutable evidence of forgery.

The Power of Document Examination

These techniques, employed by skilled investigators, serve as powerful tools in the fight against financial fraud. Through meticulous examination, they expose the deceptive nature of forged documents, ensuring the integrity of financial transactions and protecting individuals from falling prey to fraudulent schemes.