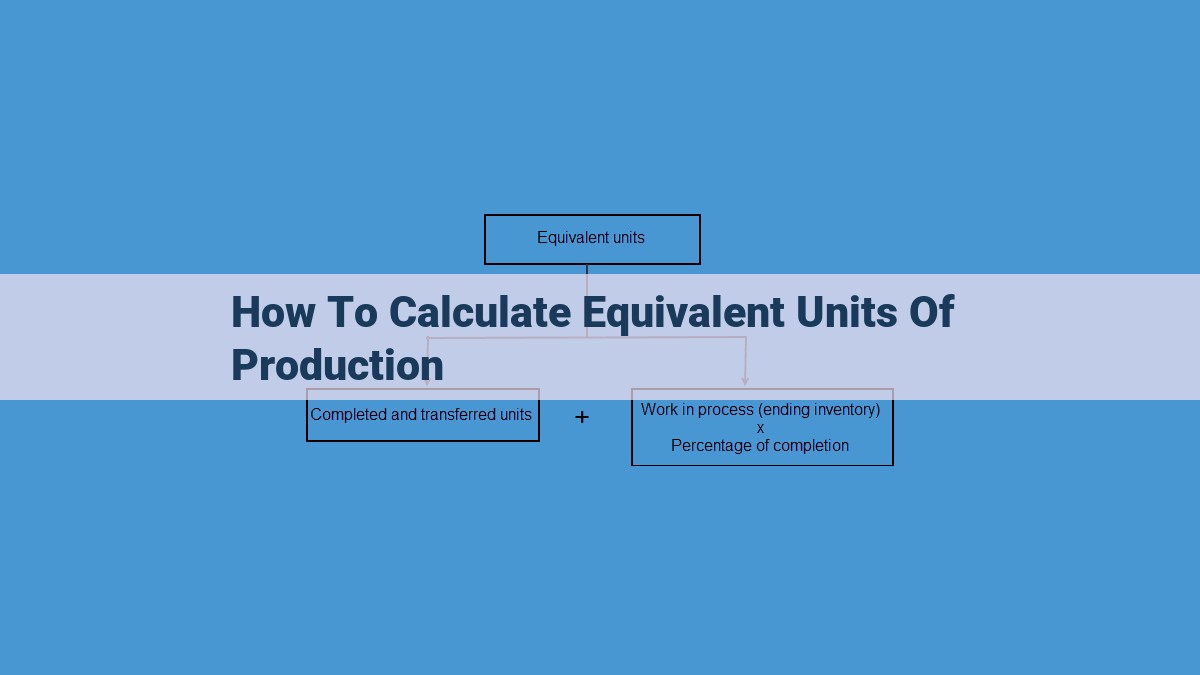

Equivalent units of production (EUP) are calculated by considering both completed units and units in progress. It measures the amount of production achieved during a period. To calculate EUP, begin with the previous period’s work in process inventory. Estimate the percentage of work completed on in-process units. Multiply the number of units by the completion percentage to determine EUP for those units. For units started during the period, calculate EUP based on the proportion of work done. Units completed and transferred out are considered fully complete, with EUP equal to their actual count.

Understanding Equivalent Units of Production (EUP)

In the realm of production and cost accounting, the concept of Equivalent Units of Production (EUP) holds significant importance. EUP serves as a yardstick to measure the production completion level achieved during a specific period, taking into account both completed units and those still in the production process.

Why is EUP crucial? It facilitates the accurate allocation of production costs across units. This precise cost allocation ensures that each product bears its fair share of the production expenses, leading to reliable financial reporting. Furthermore, EUP aids in assessing production efficiency by revealing the level of capacity utilization and highlighting areas for improvement.

To grasp the significance of EUP, it’s helpful to visualize a manufacturing scenario. Imagine a factory that produces widgets. During the month, the factory started producing 1000 widgets, completed 700, and had 300 widgets in various stages of completion at the end of the month. Using EUP, we can gauge how much production was actually completed during that month, considering both the finished units and the progress made on the in-process units.

Types of Equivalent Units

Equipping ourselves with a comprehensive understanding of Equivalent Units of Production (EUP) is paramount for ascertaining the intricacies of production accounting. EUP plays an imperative role in assigning production costs with pinpoint precision and meticulously assessing production efficiency. Typically, four distinct categories of equivalent units exist, each with its own nuances and significance.

Beginning Work in Process Inventory

Envision meticulously crafted units that have persevered through a portion of the production process at the dawn of a new accounting period. These units, nestled snugly within the beginning work in process inventory, hold immense value as they embody the cumulative labor and overhead expenses incurred upon them.

Ending Work in Process Inventory

As the curtains draw close on the current accounting period, some units may still be basking in the throes of production’s embrace. These ending work in process inventory units stand as a testament to the tireless efforts poured into their creation, awaiting their triumphant emergence as finished goods.

Units Started During the Period

Incessantly, a torrent of new units embarks upon the production journey, eager to join their brethren in the realm of completed products. These units started during the period symbolize the relentless drive of manufacturing, constantly replenishing the production pipeline.

Units Completed and Transferred Out

Finally, we bear witness to the triumphant emergence of units completed and transferred out. These units have valiantly traversed the gauntlet of production, emerging victorious as finished goods, ready to grace the shelves and satisfy eager customers.

Calculating Equivalent Units of Production: A Guide to Accuracy and Efficiency

Accurate calculation of Equivalent Units of Production (EUP) is a crucial aspect of production accounting and performance analysis. This guide will delve into the concept of EUP, its significance, and provide a step-by-step approach to its calculation.

Understanding Equivalent Units of Production

EUP measures the volume of production during a specific period, taking into account both completed and partially completed units. It is essential for allocating production costs fairly and assessing the efficiency of production processes.

Types of Equivalent Units

- Beginning Work in Process Inventory: Units carried over from the previous period that are still in production.

- Ending Work in Process Inventory: Units being worked on at the end of the period that are not yet complete.

- Units Started During the Period: New units introduced into production during the period.

- Units Completed and Transferred Out: Units finished and transferred to the next stage of production or to finished goods inventory.

Calculating Equivalent Units of Production

- Importance of Prior Period EUP: Beginning work in process inventory from the previous period is a key factor in determining total EUP.

- Determining Percent Complete: In-process units should be estimated for the percentage of work completed to calculate their EUP contribution.

- Normal EUP vs. Excess EUP: EUP can be calculated based on normal production capacity or excess production capacity. Normal EUP reflects the planned production output, while excess EUP represents production beyond normal capacity.

Applications of Equivalent Units of Production

- Production Efficiency Measurement: EUP helps assess the utilization of production resources and identify areas for improvement.

- Throughput Time Analysis: It allows for the evaluation of the time taken for units to move through the production process, highlighting bottlenecks and optimizing flow.

EUP calculation is a fundamental aspect of production management. It provides valuable insights into production cost allocation, process efficiency, and overall performance. Understanding and applying EUP effectively enables businesses to optimize production, reduce costs, and achieve greater profitability.

Applications of Equivalent Units of Production

- Production Efficiency Measurement: Describe how EUP is used to evaluate the utilization of production resources.

- Throughput Time Analysis: Explain how EUP helps in analyzing the time it takes for units to move through the production process.

Applications of Equivalent Units of Production

Understanding equivalent units of production (EUP) is crucial for accurate product costing and production analysis. By measuring the amount of production completed during a period, EUP provides insights into how effectively production resources are being utilized.

Production Efficiency Measurement

EUP plays a significant role in evaluating production efficiency. By comparing the EUP achieved to the normal EUP (based on the production capacity), businesses can identify areas for improvement. If EUP exceeds normal EUP, it indicates that production is operating beyond its usual capacity, which may lead to inefficiencies. On the other hand, if EUP falls below normal EUP, it suggests underutilization of production resources, resulting in lost production opportunities.

Throughput Time Analysis

EUP assists in analyzing throughput time – the time it takes for units to move through the production process. By comparing the EUP of completed units to the EUP of units in ending work in process inventory, businesses can determine how long units remain in production. This information can be used to identify bottlenecks, optimize production flow, and reduce lead times.

EUP calculation is essential for accurate product costing and production analysis, providing valuable insights into production efficiency and throughput time. Its applicability extends across various industries and production environments, making it a fundamental tool for improving operational performance and profitability.