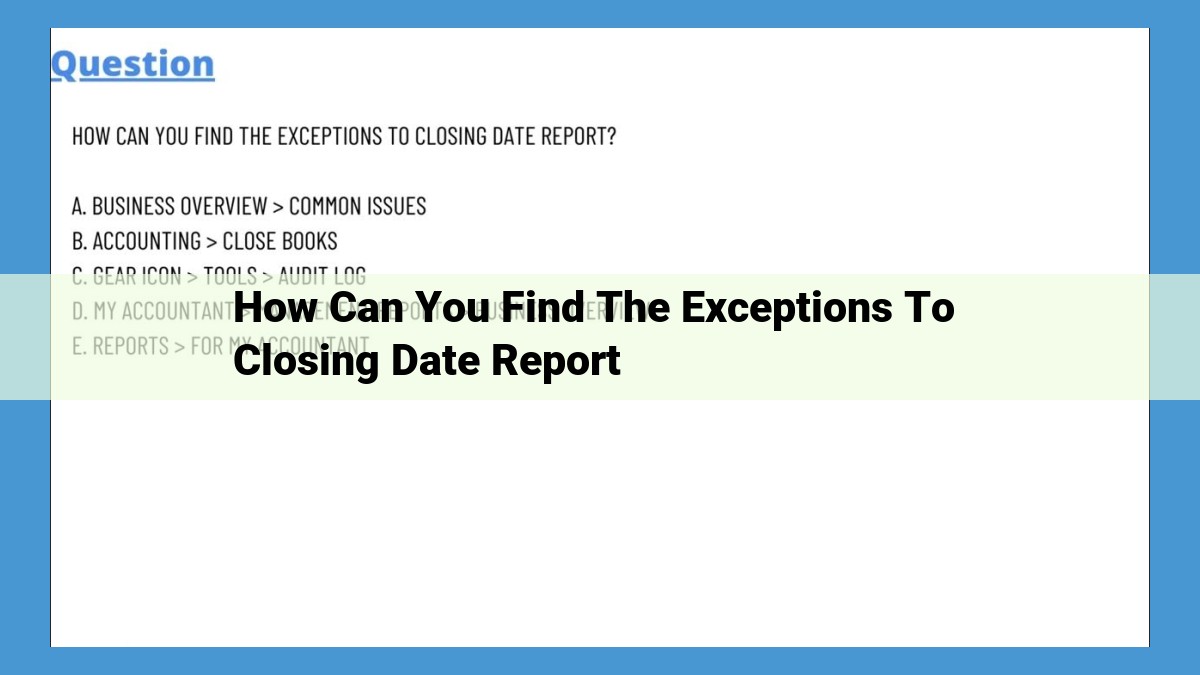

To uncover exceptions in closing date reports, follow these steps: identify unreconciled transactions, track outstanding checks, recognize deposits in transit, accrue expenses, recognize deferred revenue, record prepaid expenses, analyze loan applications, address customer disputes, resolve vendor disputes, and investigate unusual transactions. By diligently applying these measures, you will enhance the accuracy of your financial reporting and ensure compliance with accounting principles.

Bank Reconciliation: Identifying Unreconciled Transactions

Every penny counts in the world of finance. As a business or individual, keeping track of every financial transaction is crucial to maintain financial health. One important aspect of this financial housekeeping is bank reconciliation. It’s like checking your receipts against your bank statement to make sure everything matches up.

Unreconciled transactions are those discrepancies between your accounting records and your bank statement. They can be caused by various factors, such as forgetting to record transactions, posting errors, or even fraud. Identifying and resolving these discrepancies is essential to ensure the accuracy of your financial records.

So, how do we identify these pesky unreconciled transactions? It all starts with understanding what they are.

What are Unreconciled Transactions?

In simple terms, an unreconciled transaction is a financial transaction that has been recorded in one set of records (usually your accounting records) but not in another set of records (usually your bank statement). This can happen for several reasons:

-

Forgotten Transactions: You might have missed recording a transaction in your accounting software.

-

Posting Errors: You might have entered the wrong amount or posted the transaction to the wrong account.

-

Bank Errors: The bank may have made an error in processing your transaction.

-

Fraud: Unreconciled transactions can also be a sign of fraudulent activity.

Why is Bank Reconciliation Important?

Regularly reconciling your bank statement is like giving your finances a checkup. It helps you identify potential problems early on, such as:

-

Missing or duplicate payments: You can catch errors or fraud before they become major issues.

-

Overdrafts: You can identify transactions that may have caused your account to go into overdraft, helping you avoid costly fees.

-

Stolen funds: In case of fraud, bank reconciliation can help you detect unauthorized transactions.

Next Steps in the Journey

In the next section, we’ll delve into the practical steps involved in identifying and resolving unreconciled transactions. Stay tuned!

Identifying Unreconciled Transactions: The Key to Accurate Financial Reporting

Bank Reconciliation: A Crucial Step for Financial Accuracy

Regularly reconciling your bank statements is essential for maintaining the accuracy of your accounting records. By comparing your bank statement with your accounting records, you can identify any discrepancies and ensure that your books reflect the actual cash flow of your business.

Unreconciled Transactions: A Sign of Potential Errors

Unreconciled transactions are financial transactions that have not been recorded in both your accounting records and bank statement. These discrepancies can arise due to various reasons, such as delayed deposits, outstanding checks, or unrecorded expenses.

Tracking Outstanding Checks: Ensuring Accuracy

Outstanding checks are payments that have been issued but not yet cashed by the recipient. By tracking outstanding checks and reconciling them with your bank statement, you can avoid overstating your cash balance. This process ensures that your accounting records accurately reflect the actual funds available in your bank account.

Deposits in Transit: Recording Earned Revenue

Deposits in transit are payments received but not yet reflected in your bank statement. Failure to record these deposits can lead to an overstatement of your revenue. By identifying and recording deposits in transit, you ensure that your financial statements accurately reflect the revenue earned during the accounting period.

Accruing Expenses: Matching Principle and Accurate Liabilities

Accrued expenses are expenses that have been incurred but not yet paid. The matching principle of accounting requires that these expenses be recognized in the same period they are incurred, regardless of payment date. By accruing expenses, you ensure that your financial statements accurately reflect your company’s true liabilities.

Recognizing Deferred Revenue: Avoiding Overstatement

Deferred revenue is revenue received in advance for services or products not yet delivered. By recognizing deferred revenue, you prevent an overstatement of your revenue. This approach ensures that your financial statements accurately reflect the revenue earned during the accounting period.

Recording Prepaid Expenses: Improving Cash Flow Analysis

Prepaid expenses are expenses that have been paid in advance for future use. Recording these expenses allows you to better analyze your cash flow. By understanding how prepaid expenses impact your cash flow, you can make more informed financial decisions.

Identifying discrepancies between accounting records and bank statements

Identifying Discrepancies Between Accounting Records and Bank Statements: A Crucial Step in Financial Reconciliation

Financial reconciliation is a fundamental accounting process that ensures the accuracy and integrity of your financial records. By comparing your accounting records to your bank statements, you can identify and correct discrepancies that may have occurred during the accounting period. One key aspect of reconciliation is identifying discrepancies between your accounting records and bank statements.

Discrepancies can arise for various reasons, such as unrecorded transactions, processing errors, and fraudulent activities. It is essential to investigate and resolve these discrepancies promptly to maintain the accuracy and reliability of your financial records.

Unrecorded Transactions:

Unrecorded transactions occur when a transaction is processed in your accounting system but not reflected in your bank statement. These can include unrecorded deposits, unrecorded checks, or adjusting entries that have not been recorded.

Processing Errors:

Processing errors can occur during the recording, posting, or reconciliation process. These errors can be caused by human mistakes, software glitches, or misinterpretations.

Fraudulent Activities:

Fraudulent activities such as unauthorized withdrawals or deposits, forged checks, or theft of funds can also lead to discrepancies between your accounting records and bank statements.

Steps to Identify Discrepancies:

- Compare your check register to your bank statement: Look for uncleared checks and identify any checks that have cleared but are not recorded in your accounting system.

- Review your deposits: Ensure that all deposits recorded in your accounting system are reflected in your bank statement. Investigate any discrepancies between the amounts and dates.

- Analyze bank fees and other charges: Compare the bank fees and charges on your bank statement to those recorded in your accounting system. Identify any discrepancies and determine the cause.

- Investigate returned items: If you receive a notice of a returned check or direct deposit, investigate the reason for the return and ensure that the transaction is properly recorded in your accounting system.

- Review your accounting entries: Check your accounting entries for any errors or omissions that may have caused discrepancies with your bank statement.

By diligently identifying and resolving discrepancies between your accounting records and bank statements, you can safeguard your financial data, prevent errors, and ensure the accuracy of your financial reporting. Accurate financial records are crucial for informed decision-making, regulatory compliance, and maintaining investor confidence.

The Power of Bank Reconciliation: Uncovering Hidden Cash Flow Truths

reconciling your bank statements is like digging through a treasure trove, uncovering valuable insights to empower your financial decision-making. Imagine a world where your cash flow is so clear, you can predict your financial future with ease. Bank reconciliation holds the key to unlocking this clarity.

Identifying Uncashed Checks: A Cash Flow Lifeline

Bank reconciliation helps you track down uncashed checks like a financial detective. These forgotten funds can be lurking in your system, leaving you with an inaccurate picture of your cash flow. By diligently identifying and reconciling these outstanding checks, you’ll have a clearer understanding of your available funds, allowing you to make informed decisions about your spending.

Benefits that Make Bank Reconciliation a Cash Flow Game-Changer

- Enhances the accuracy of your financial records, so you can trust the numbers you’re working with.

- Prevents the overstatement of expenses, ensuring you don’t overspend or miss out on potential savings.

- Helps you keep tabs on your cash flow, enabling you to make strategic decisions and stay ahead of potential cash flow crunches.

- Provides peace of mind, knowing that your finances are in order and that you’re not missing any crucial information.

Embrace the power of bank reconciliation and embark on a journey of financial clarity. With each reconciled transaction, you’ll uncover hidden truths, empowering you to make informed decisions that will drive your business to success.

Identifying Uncashed Checks: A Crucial Step for Accurate Reconciliations

Reconciling bank statements and accounting records is essential for maintaining financial accuracy. Uncashed checks represent a common discrepancy that can lead to errors. Identifying and reconciling these checks is crucial to ensure your books are up-to-date and reflect the true financial position of your business.

Uncashed checks are typically checks that have been issued but not yet presented for payment by the recipient. This can occur for various reasons, such as the recipient holding onto the check for a period of time or it being lost in transit.

Benefits of Tracking Outstanding Checks:

- Accurate reconciliation of bank statements: Prevents overstatement or understatement of cash balances.

- Timely follow-up: Helps identify checks that may have been lost or stolen, allowing for timely action.

- Improved cash flow analysis: Provides insight into the timing of payments and cash availability.

Identifying Uncashed Checks:

- Compare outstanding checks: Regularly review the list of outstanding checks with your bank statement to identify checks that have cleared.

- Use a check reconciliation software: This can automate the process, making it more efficient and accurate.

- Contact customers: Politely inquire about the status of outstanding checks that have been issued for a significant period of time.

Reconciling Outstanding Checks:

- Record cleared checks: Mark those that have cleared as such in your accounting records to avoid double-counting.

- Void uncashed checks: If a check remains uncashed for an extended period, it should be voided and re-issued.

- Adjust cash balance: Reconcile the difference between the book balance and bank balance to account for outstanding checks.

By identifying and reconciling uncashed checks, you can maintain the accuracy of your accounting records and ensure a clear understanding of your company’s financial position. Regular monitoring and timely follow-up are essential for successful check reconciliation and optimal financial management.

**Reconciling Outstanding Checks to Ensure Accuracy**

It’s like a detective story in the world of accounting. When those checks you’ve written don’t disappear from your bank statement, it’s time to embark on a mission to find the missing pieces.

Identifying the Mystery: What Are Outstanding Checks?

Outstanding checks are those that have been issued but not yet cashed. They represent a liability for your company until they’re cleared. Mismanaging them can lead to an inaccurate picture of your cash flow and overstating your expenses.

The Importance of Reconciliation

Reconciling outstanding checks is crucial because it ensures that your accounting records match reality. It helps you:

- Verify that all checks have been cleared or processed

- Identify any errors in recording check payments

- Maintain an accurate balance in your bank account

Unveiling the Clues: Finding Uncashed Checks

The first step is to compare your accounting records to your bank statement. Look for any checks that have been issued but not yet marked as cleared. These are your outstanding checks.

Connecting the Dots: Matching Checks to Transactions

Once you’ve identified the outstanding checks, you need to determine which transactions they represent. Review your purchase orders, invoices, and other supporting documentation to match the checks to the expenses they paid for.

Resolving the Discrepancy: Clearing the Checks

Finally, you need to clear the outstanding checks from your accounting system. This means recording the checks as cleared in your accounting software and updating your bank reconciliation.

By following these steps, you can ensure that your outstanding checks are properly reconciled, providing you with a clear and accurate picture of your company’s financial health.

Unveiling the Mysteries of Deposits in Transit

In the realm of accounting, deposits in transit are the unsung heroes that ensure accurate financial reporting. These are deposits that have been made to a company’s bank account but have not yet been recorded in its accounting records. Identifying and recording them is crucial to prevent revenue overstatement.

Deposits in transit arise due to the time lag between when a customer makes a deposit and when the bank processes it. This time delay can vary depending on factors such as the payment method, bank processing times, and weekends or holidays. As a result, deposits may be reflected on the bank statement but not yet captured in the company’s accounting system.

Ignoring deposits in transit leads to overstating revenue in the current period. This is because the company has received the money from customers but has not yet recognized it as income. Correctly recording deposits in transit ensures that revenue is recognized in the appropriate period, providing a truer picture of the company’s financial performance.

Why Identifying Deposits in Transit Is Crucial for Accurate Accounting

Picture this: Your business has been thriving, and you’re confident that your books are in order. But during a routine bank reconciliation, you stumble upon a discrepancy—deposits in transit. What are they, and why is it so important to identify them?

Deposits in transit are payments received by your business but not yet recorded in your bank account. They can occur when customers pay by check or make online transfers that take a few days to process. If these deposits are not recognized, it can lead to a revenue overstatement in your financial records.

Why is this a problem? Because it can misrepresent your business’s financial health. Overstated revenue can result in inaccurate cash flow projections, improper tax filings, and difficulty securing loans. To avoid these pitfalls, it’s crucial to identify and account for deposits in transit.

By tracking these deposits, you can ensure that your records accurately reflect the income your business has earned, even if it hasn’t yet hit your bank account. This transparency allows you to make informed decisions about your finances, stay compliant with regulations, and protect your business’s reputation.

So, how do you identify deposits in transit? Regularly reconcile your bank statements with your accounting records. Look for payments that have been recorded in your books but not in your bank account. These are likely deposits in transit. By promptly recording these deposits, you can eliminate revenue discrepancies and maintain the integrity of your financial statements.

Identifying Deposits in Transit: The Key to Accurate Revenue Recognition

In the realm of accounting, reconciling bank statements is a crucial practice that helps businesses ensure the integrity of their financial records. One of the key components of bank reconciliation is identifying deposits in transit. These are deposits that have been made to a company’s bank account but have not yet been recorded in their accounting system.

Deposits in transit arise when customers make payments towards their invoices, which are then deposited into the company’s bank account. However, these deposits may not be reflected in the accounting records immediately, as they take time to process through the banking system.

Failure to recognize deposits in transit can lead to an overstatement of revenue. This is because the company’s accounting records would show a lower balance than the actual amount of cash received. This can have a negative impact on the company’s financial statements, as it can inflate their reported profits and assets.

Therefore, it is essential for businesses to have a system in place to identify and record deposits in transit promptly. This can be achieved through regular bank statement reconciliations, which involve comparing the bank statement to the company’s accounting records and identifying any discrepancies. By keeping close track of deposits in transit, businesses can ensure that their financial records accurately reflect their true financial performance.

Explanation of accrued expenses

Accruing Expenses: Ensuring Accurate Financial Reporting

Imagine a small business owner, let’s call him John, who is meticulous about record-keeping. Yet, when it comes to financial reporting, he often finds himself puzzled by discrepancies between his business’s income and expenses. This issue stems from his oversight of a crucial accounting principle: the matching principle.

The matching principle dictates that expenses should be recognized in the same period as the revenue they generate. This ensures that a business’s financial statements accurately reflect its economic activity. Without adhering to this principle, John’s business would likely overstate its expenses in one period and understate them in another, leading to distorted financial data.

To resolve this issue, John must embrace the concept of accrued expenses. Accrued expenses are expenses that have been incurred but not yet paid. They represent obligations that the business currently owes but will only be paid in the future. For instance, if John’s business uses electricity but has not yet received an invoice, the cost of that electricity is an accrued expense.

By recognizing accrued expenses, John can ensure that his financial statements portray a true picture of his business’s expenses. This allows him to make informed decisions about pricing, cash flow, and profitability. It also prevents his business from understating its liabilities, which could have negative implications for financial performance and stakeholder confidence.

The Importance of Matching Principle in Accounting: Ensuring Accurate Financial Reporting

In the realm of accounting, precision is paramount. The matching principle stands as a cornerstone of this accuracy, ensuring that expenses are recognized in the same period as the revenue they generate. This fundamental concept underpins the integrity of financial reporting and provides a clear picture of a company’s financial performance.

The matching principle dictates that expenses should be recognized when they are incurred, regardless of when payment is made. By aligning expenses with the related revenue, accountants can accurately measure the profitability of a period and avoid distorting the financial statements.

Imagine a company that sells products on credit. If the company records revenue when the sale is made but waits until payment is received to record the related cost of goods sold, the company’s financial statements will overstate its profitability in the period of the sale. This is because the expenses incurred to generate that revenue have not yet been recognized.

By following the matching principle, the company would recognize the cost of goods sold in the same period as the revenue. This ensures that the company’s financial statements accurately reflect its performance and provide a true representation of its financial position.

The matching principle ensures that expenses are matched to the revenue they generate, providing a complete and accurate view of a company’s financial performance. By adhering to this principle, accountants can ensure the integrity of financial reporting and provide stakeholders with a reliable basis for making informed decisions.

Accruing Expenses: Ensuring Accuracy in Financial Reporting

In the intricate world of accounting, navigating various financial transactions can be akin to navigating a maze. One crucial aspect that plays a pivotal role in presenting a true and fair view of a company’s financial position is the concept of accruing expenses. This accounting practice requires businesses to recognize expenses that have been incurred but not yet paid.

Accruing expenses is an integral part of financial reporting under the matching principle. This principle dictates that expenses should be matched to the revenues they generate, regardless of when the cash payment is made. By accruing expenses, businesses ensure that their financial statements accurately reflect the company’s financial performance for a specific period.

Why is Accruing Expenses Important?

Accruing expenses serves several key purposes. It prevents companies from overstating their net income by only recognizing expenses when they are paid in cash. This is crucial because it ensures that the true cost of goods sold and operating expenses are reflected in the income statement for the appropriate period.

Additionally, accruing expenses helps businesses avoid understating their liabilities. By recognizing expenses as they are incurred, companies can accurately depict their financial obligations and ensure that adequate provisions are made for future payments. This enhanced accuracy is especially important for creditors and investors who rely on financial statements to make informed decisions.

How to Accrue Expenses

The process of accruing expenses involves several steps. First, businesses need to identify all expenses that have been incurred but not yet paid. This may include expenses such as salaries, rent, and utilities. Once expenses are identified, the amount of the expense is estimated and recorded as an expense in the income statement. A corresponding liability account is also created on the balance sheet to reflect the obligation to pay the expense in the future.

Real-World Example

Let’s consider a scenario to illustrate the importance of accruing expenses. Imagine a manufacturing company that produces and sells widgets. In January, the company incurs $10,000 in salary expenses for employees who worked during the month. However, the company’s payroll date is on the 5th of the following month.

If the company fails to accrue expenses, its income statement for January will only reflect the salaries that have been paid as of the end of the month. This would result in an understatement of expenses and an overstatement of net income. To ensure accuracy, the company should accrue the $10,000 in salary expenses in January, even though the cash payment will not be made until February. This ensures that the income statement for January reflects the true cost of producing and selling widgets during the month.

In conclusion, accruing expenses is a crucial accounting practice that ensures the accurate and transparent reporting of a company’s financial performance. By recognizing expenses when they are incurred, businesses can avoid overstating their profits and understating their liabilities. This enhances the credibility and reliability of financial statements, which is essential for decision-making by stakeholders, creditors, and investors.

Deferred Revenue: Unveiling the Secrets of Accrual Accounting

In the world of accounting, it’s not always straightforward to determine how much money you’ve truly earned. That’s where deferred revenue comes into play. It’s like a secret stash of income that’s waiting to be released into your hungry coffers.

What’s Deferred Revenue?

Deferred revenue, also known as unearned income, is the amount of money you’ve received upfront for services or products that you haven’t yet delivered. It’s like a membership fee for a gym. You pay the money today, but you get to enjoy the sweat and endorphins later.

Why is it Important to Recognize Deferred Revenue?

Recognizing deferred revenue is like keeping your financial books in order. It prevents you from overstating your income and painting a rosier picture than reality. By recognizing deferred revenue, you’re ensuring that you’re accurately reporting your earnings, aligning them with the services you’ve actually performed.

How to Recognize Deferred Revenue

To recognize deferred revenue, you need to be able to identify it. Look for transactions where you’ve received payment in advance for goods or services you haven’t yet provided. Once you’ve spotted these gems, record them as a liability on your balance sheet. This way, you’ll have a clear record of the obligations you have to your customers.

Benefits of Recognizing Deferred Revenue

Recognizing deferred revenue is like giving your financial statements a superpower. It helps you:

- Accurately match revenue to expenses: By recognizing revenue as you earn it, you can ensure that your expenses are properly matched to the revenue they generate. This gives you a clearer picture of your profitability.

- Avoid inflated income statements: Overstating your income can lead to trouble with investors and tax authorities. Deferred revenue ensures your income reports are true and fair.

- Improve financial planning: Knowing how much deferred revenue you have can help you plan for the future. You can estimate future cash flow and make informed decisions about staffing and operations.

So, there you have it. Deferred revenue: the not-so-secret key to accurate and reliable financial reporting. By recognizing deferred revenue, you’re not only protecting your company’s reputation, but you’re also making sure your financial statements are as fit as a fiddle.

The Vital Role of Deferred Revenue in Preventing Financial Overstatement

Imagine running a business and discovering a discrepancy between your accounting records and bank statements. It’s a common occurrence that can lead to serious financial problems if not handled promptly and accurately. One key factor to consider in this scenario is deferred revenue.

Deferred revenue refers to income that has been received but not yet earned. This typically occurs when a customer pays in advance for goods or services that will be delivered or performed in the future. Recognizing deferred revenue is crucial because it prevents revenue overstatement, ensuring that your financial statements accurately reflect your company’s financial performance.

Benefits of Recognizing Deferred Revenue

- Accurate Financial Reporting: By recording deferred revenue, you create a true picture of your financial position. This is essential for investors, creditors, and other stakeholders to make informed decisions about your business.

- Compliance with Accounting Standards: Generally Accepted Accounting Principles (GAAP) require companies to recognize deferred revenue. Ignoring this requirement can lead to audit failures and legal consequences.

- Avoidance of Overstating Income: By recognizing deferred revenue, you avoid the temptation to book income before it has been earned. This prevents artificial inflation of your revenue and subsequent misleading financial statements.

- Improved Cash Flow Management: Deferred revenue provides a buffer between cash received and actual revenue earned. This can help you plan for future cash flows and avoid relying heavily on short-term financing.

- Enhanced Business Stability: Accurate financial reporting, supported by the proper recognition of deferred revenue, contributes to business stability and reduces the risk of financial shocks.

Recognizing Deferred Revenue to Prevent Overstatement

Don’t Fall for the Revenue Trap: Recognize Deferred Revenue

In the world of accounting, it’s easy to get caught up in the excitement of recognizing revenue. After all, it makes your company look like a financial superstar, right? But hold your horses there, partner. If you’re not careful, you could end up overstating your revenue and painting a rosy picture that’s far from reality. That’s where deferred revenue comes in, my friend.

Deferred revenue is like a futuristic piggy bank. It’s revenue that you’ve earned but haven’t yet received. Think of it as a promise from your customers that they’ll cough up the dough in the future. Recognizing this revenue is crucial because it prevents you from inflating your current income and gives you a more accurate snapshot of your financial health.

For instance, let’s say you sell a subscription for access to your exclusive online content. The customer pays $120 upfront for a one-year subscription. Instead of recognizing all $120 as revenue right away, you’d record it as deferred revenue. This is because you haven’t actually earned all of that money yet. Over the next 12 months, as the customer accesses your content, you’ll gradually recognize that deferred revenue as earned revenue.

By recognizing deferred revenue, you’re matching revenue to the actual period when it’s earned. This helps you avoid overstating your income and provides a more reliable basis for your financial statements. So, remember, my accounting pal, don’t fall into the revenue trap. Embrace the power of deferred revenue to paint a clear and accurate picture of your company’s financial performance.

Definition of prepaid expenses

Managing the Elusive Nature of Prepaid Expenses: A Guide to Improved Cash Flow Analysis

In the intricate realm of accounting, there exists a concept known as prepaid expenses, an often-overlooked factor that can significantly impact your cash flow analysis. Prepaid expenses represent those costs incurred in advance for goods or services that have yet to be consumed or utilized.

Picture this: your company pays for an annual insurance premium in January. However, the insurance coverage extends from February 1 to January 31 the following year. In this scenario, only a portion of the premium relates to the current accounting period, which ends on December 31. The remaining portion represents a prepaid expense that must be recognized and allocated over the duration of the coverage period.

Recognizing prepaid expenses is not only crucial for maintaining accurate financial reporting but also plays a pivotal role in effective cash flow management. By properly recording these expenses, businesses can gain valuable insights into their cash flow patterns and make informed decisions regarding future spending and operations.

Failure to account for prepaid expenses can lead to an overstatement of current-period expenses, potentially resulting in a distorted view of your company’s financial health. Conversely, overstating prepaid expenses can also impact your balance sheet by inflating current assets, which may have unintended consequences when it comes to calculating financial ratios and seeking external financing.

By embracing diligent management of prepaid expenses, you empower yourself with the knowledge of true cash flow patterns, enabling you to anticipate future cash needs, negotiate payment terms with suppliers, and make strategic investments that drive your business forward.

Recording Prepaid Expenses: Enhancing Cash Flow Analysis

In the bustling world of accounting, meticulously recording financial transactions is paramount to ensuring accuracy and transparency. Among these transactions, prepaid expenses often go unnoticed, yet they play a crucial role in cash flow analysis and the overall financial health of a business.

What Are Prepaid Expenses?

Prepaid expenses are outlays made by a company in advance for goods or services that will be received or consumed in the future. They represent a temporary decrease in cash, but they will eventually be recognized as an asset as the goods or services are received. Common examples include insurance premiums, rent, and supplies.

Importance of Recording Prepaid Expenses

Recording prepaid expenses is essential for several reasons:

- Accurate Financial Reporting: Failing to record prepaid expenses can overstate expenses in the current period and understate assets, providing a distorted view of the company’s financial performance.

- Improved Cash Flow Analysis: Prepaid expenses affect both the cash flow statement and the balance sheet. Recording them accurately helps track cash inflows and outflows and allows businesses to better forecast their future financial needs.

- Compliance with Accounting Standards: Most commonly accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS) require companies to record prepaid expenses in the period in which they are paid. Failure to do so may result in non-compliance.

How Prepaid Expenses Affect Cash Flow Analysis

Prepaid expenses initially reduce cash flow when they are paid upfront. However, as the goods or services are received and consumed, the expenses are gradually recognized on the income statement, which reduces future cash outflows. By recording prepaid expenses accurately, businesses can better understand their cash flow patterns and make informed decisions about future investments and expenses.

Recording prepaid expenses is a crucial aspect of accounting that not only ensures accurate financial reporting but also enhances cash flow analysis. By diligently tracking and recording these expenses, businesses can gain a clearer understanding of their financial situation, make informed decisions, and ultimately optimize their performance.

How Prepaid Expenses Impact Cash Flow Analysis

Understanding cash flow is crucial for any business. It’s the lifeblood of your company, and it’s essential to know where your money is coming from and going to. Prepaid expenses can significantly impact your cash flow analysis, and it’s important to understand how they work.

Definition of Prepaid Expenses

Prepaid expenses are expenses that you pay upfront for goods or services that you haven’t yet received. For example, if you pay your insurance premium for the year in advance, this would be considered a prepaid expense.

Recording Prepaid Expenses

When you record a prepaid expense, you debit the prepaid expense account and credit the cash account. This will increase your prepaid expense balance and decrease your cash balance.

Impact on Cash Flow Analysis

Prepaid expenses can have a negative impact on your cash flow analysis in the short term. This is because you’re paying for a good or service that you haven’t yet received. However, in the long term, prepaid expenses can actually improve your cash flow. This is because you’re spreading the cost of the expense over the period of time that you’re using the good or service.

For example, let’s say you pay $1,200 for a year’s worth of insurance. This would be recorded as a prepaid expense. In the first month, your cash flow would be reduced by $1,200. However, over the course of the year, you would gradually use up the prepaid expense. This would mean that your cash flow would only be reduced by $100 each month.

Prepaid expenses can be a valuable tool for managing your cash flow. By understanding how they work, you can use them to your advantage.

Tracking Loan Applications: A Window into Future Performance

Every loan application is a step towards a company’s financial growth, a chance to expand operations, invest in new ventures, and unlock opportunities. But beyond the immediate excitement lies a crucial need to track these applications diligently, for they hold valuable insights into a company’s future performance.

By monitoring the progress of loan applications, companies can gain a clearer understanding of their financial trajectory, identify potential risks, and make informed decisions that can shape their destiny.

Tracking loan applications is like keeping a pulse on a company’s financial health. It allows companies to assess the likelihood of loan approvals, predict cash flow, and evaluate the impact of loans on their bottom line. This foresight empowers companies to plan strategically, allocate resources effectively, and mitigate any potential obstacles.

Furthermore, tracking loan applications provides a window into a company’s creditworthiness. Lenders meticulously scrutinize loan applications to assess a company’s ability to repay the loan, its financial stability, and its overall risk profile. By keeping a close eye on loan application progress, companies can identify areas where they can improve their creditworthiness and increase their chances of securing favorable loan terms.

In essence, tracking loan applications is not merely an administrative task; it’s an essential practice that helps companies stay on top of their financial goals and navigate the path to success. It’s a proactive approach to risk management and a powerful tool for shaping the future of any business.

Evaluating potential impact of loans on financial performance

Evaluating the Potential Impact of Loans on Financial Performance: A Tale of Growth and Strategy

In the realm of finance, accessing loans can be a pivotal decision for any organization. While loans provide the necessary capital for expansion and growth, they also come with certain financial implications that must be carefully evaluated.

One crucial aspect to consider is the potential impact of loans on your organization’s financial performance. By delving into the details of loan applications in process, you can arm yourself with valuable insights that will shape your future decision-making.

The Loan Landscape: A Two-Edged Sword

Loans can be a double-edged sword. On the one hand, they provide the much-needed financial boost for investing in new ventures, upgrading equipment, or expanding into new markets. This can translate into increased sales, improved cash flow, and enhanced profitability.

On the other hand, loans also introduce additional financial obligations in the form of interest payments and principal repayments. These obligations can put pressure on your organization’s budget, potentially affecting profitability and cash flow. It’s imperative to strike a delicate balance between leveraging loan capital for growth while maintaining financial stability.

Delving into the Loan Applications

To fully comprehend the potential impact of loans, it’s essential to analyze loan applications in process. These applications provide a wealth of information that can help you assess the feasibility and viability of proposed projects.

- Purpose of the Loan: Determine the intended use of the loan proceeds. This will give you an indication of the areas where your organization plans to invest, which in turn can shed light on potential growth opportunities.

- Loan Amount and Terms: Understand the total amount of the loan, its term (i.e., duration), and the interest rate. These factors will directly affect your organization’s financial obligations and overall cost of borrowing.

- Financial Projections: Review the financial projections submitted with the loan application. These projections provide insights into the expected financial performance of the project, including revenue, expenses, and profitability. By evaluating these projections, you can assess the potential impact on your organization’s financial health.

Forecasting the Future: Unraveling the Impact

The insights gained from analyzing loan applications can serve as a powerful tool for forecasting the future impact on your organization’s financial performance.

- Impact on Cash Flow: Assess how the loan will affect your organization’s cash flow. Consider the timing of loan disbursements and repayments, as well as the impact of interest payments on your cash reserves.

- Profitability Analysis: Determine the potential impact of the loan on your organization’s profitability. Consider the projected revenue and expenses associated with the project, and evaluate how these factors will affect your bottom line.

- Liquidity Management: Evaluate the impact of the loan on your organization’s liquidity. Consider the potential need for additional financing to cover loan obligations or unexpected expenses, and assess your organization’s ability to meet these needs.

By carefully evaluating the potential impact of loans on financial performance, you can make informed decisions that align with your organization’s strategic goals. This proactive approach will help you harness the power of debt financing for growth while mitigating potential risks and safeguarding your organization’s financial stability.

Analyzing Loan Applications in Process for Future Performance

In the competitive world of lending, identifying factors that may influence loan approval is crucial for businesses to make informed decisions and maximize loan acquisition. When reviewing loan applications, there’s a plethora of factors lenders meticulously analyze to determine their prospects. Understanding these key elements can help you strategically position your business for loan approval.

1. Credit History and Score:

Like a report card for your financial behavior, your credit history and score hold immense weight in loan approval. Lenders scrutinize this data to assess your ability to repay the loan, based on your previous payment patterns and any outstanding debts. Maintain a solid credit history and strive for a high credit score to increase your chances.

2. Financial Statements and Stability:

Your financial statements unveil the financial health of your business. Lenders seek evidence of stable revenue, profitability, and cash flow. They want to know you have the capacity to repay the loan without financial distress. Provide clear and accurate financial records that demonstrate your business’s resilience and growth potential.

3. Industry Outlook and Business Model:

The industry in which your business operates plays a role in loan approval. Lenders prefer industries with stable growth prospects and those that align with their risk appetite. Additionally, a well-defined and sustainable business model showcases your ability to generate revenue and navigate market challenges.

4. Management Team and Experience:

The experience and capabilities of your management team are also considered. Lenders seek individuals with a proven track record in managing businesses successfully. Demonstrate the expertise and leadership of your team in your loan application.

5. Loan Purpose and Collateral:

Clearly outline the purpose of your loan request and provide sufficient documentation. Lenders want to know how the loan will benefit your business and how you plan to use it. Additionally, offering collateral to secure the loan can increase your approval odds.

By understanding and addressing these factors, you can present a compelling loan application that increases your chances of loan approval. Remember, the lending process is a partnership, and open communication and a tailored approach can lead to a successful outcome.

Understanding Customer Disputes: A Guide to Protecting Revenue

Defining Customer Disputes: A Costly Conundrum

Customer disputes are a common occurrence in any business, arising from discrepancies in product quality, delivery issues, or billing errors. These disputes can have a significant impact on revenue and damage customer relationships.

The Revenue Impact: A Leaky Faucet

When a customer disputes a purchase, the revenue associated with that transaction is put on hold until the dispute is resolved. This can lead to temporary cash flow issues and hinder your ability to meet financial obligations. Moreover, if disputes are not handled promptly and effectively, they can escalate into chargebacks, resulting in permanent revenue loss and associated fees.

Protecting Customer Relationships: A Balancing Act

Unresolved customer disputes can quickly erode customer trust and loyalty. Dissatisfied customers may leave negative reviews, damage your brand reputation, and even switch to competitors. It’s crucial to address disputes quickly and fairly to maintain a positive customer experience and protect your revenue stream.

Dispute Resolution: A Delicate Dance

Effectively resolving customer disputes requires a balanced approach. Listen attentively to the customer’s perspective, investigate the issue thoroughly, and be willing to compromise if necessary. Clear communication and timely updates will keep the customer informed and reduce the risk of disputes escalating into legal or financial quagmires.

By understanding the definition and potential impact of customer disputes, businesses can develop proactive strategies to minimize their occurrence, resolve them efficiently, and protect their revenue and reputation. Remember, customer disputes are not just an inconvenience; they are an opportunity to strengthen your relationships and safeguard your financial well-being.

The Impact of Customer Disputes on Revenue: A Case Study

In the realm of finance, even the most meticulous record-keeping can’t fully shield businesses from the unexpected. Customer disputes are a common occurrence that can have a significant impact on revenue, disrupting the smooth flow of operations.

Imagine yourself as the financial manager of a thriving e-commerce company. One day, you notice a spike in customer disputes related to a particular batch of products. Customers are claiming that the products are defective and demanding refunds. Initially, you dismiss it as a minor inconvenience, but as the number of disputes grows, so does your concern.

Upon further investigation, you discover a pattern in the complaints. The products in question were recently purchased from a new supplier. Eager to expand your product line, you moved forward with the purchase despite some reservations about the supplier’s reliability.

Now, the consequences of your decision are becoming all too apparent. The faulty products are not only damaging your company’s reputation but also eroding your revenue. You realize that you must act swiftly to resolve the disputes and minimize the damage.

You reach out to the supplier, who initially denies responsibility, blaming the customers for misuse. However, after presenting irrefutable evidence, the supplier reluctantly agrees to take back the defective products and issue refunds.

The resolution process is not without its challenges. Some customers are reluctant to return the products, while others demand compensation for their inconvenience. You work tirelessly to address each dispute fairly and professionally, prioritizing customer satisfaction.

Finally, after weeks of negotiations and concessions, you manage to settle the disputes amicably. The faulty products are returned, refunds are issued, and the customer relationships are restored. However, the financial toll on your company is undeniable.

The cost of the refunds and compensation, combined with the loss of sales due to negative publicity, has significantly reduced your revenue. You learn a valuable lesson about the importance of thoroughly vetting suppliers and the potential pitfalls of rushing into new business relationships.

From this experience, you emerge with a renewed appreciation for the impact of customer disputes on revenue. You implement stricter quality control measures and establish a dedicated team to handle customer inquiries promptly and effectively. By being proactive and responsive, you aim to prevent future disputes from escalating into revenue-draining crises.

Resolving Disputes to Improve Customer Satisfaction: A Path to Customer Loyalty

Every business strives to build a strong and loyal customer base. However, disputes and disagreements inevitably arise along the way. These conflicts can potentially damage customer relationships and lead to lost revenue if not handled effectively. Embracing a proactive approach to dispute resolution is crucial in safeguarding customer satisfaction and fostering a positive customer experience.

The Impact of Customer Disputes

Customer disputes can manifest in various forms, from product quality concerns to billing issues. Unresolved disputes can erode trust, damage a company’s reputation, and divert valuable time and resources. Moreover, negative customer feedback can spread through social media and online reviews, further tarnishing a business’s image.

The Art of Dispute Resolution

Resolving customer disputes effectively requires a combination of empathy, communication, and problem-solving skills. It starts with acknowledging the customer’s concerns and actively listening to their perspective. “Understanding their pain points” helps tailor a solution that addresses their specific needs.

Effective communication is the cornerstone of dispute resolution. “Clear and transparent communication” allows customers to feel heard and valued. Regularly updating them on the progress and possible outcomes fosters a sense of trust and collaboration.

Finally, devising a mutually acceptable solution is the ultimate goal. This may involve exchanging goods, providing refunds, or offering compensation. It’s important to “be fair and reasonable” while also protecting the company’s interests.

Benefits of Dispute Resolution

Resolving disputes efficiently and amicably has numerous benefits for businesses. Improved customer satisfaction leads to increased customer loyalty, repeat business, and positive word-of-mouth marketing. “Happy customers become advocates for a brand“, leaving favorable reviews and recommending products or services to others.

Additionally, prompt dispute resolution can prevent disputes from escalating into costly legal battles or negative publicity. By proactively addressing customer concerns, businesses can “minimize the potential for damage” and focus on building stronger customer relationships.

Customer disputes are an inevitable part of business. However, with the right approach, disputes can be transformed into opportunities to strengthen customer satisfaction and loyalty. By acknowledging concerns, communicating effectively, and striving for mutually acceptable solutions, businesses can build lasting relationships with their customers and protect their reputation in the process.

Defining vendor disputes

Protecting Company Interests: Resolving Vendor Disputes

Vendor disputes are disagreements between a company and its vendors over goods or services provided. These disputes can arise for various reasons, such as incorrect billing, defective products, or undelivered orders. Resolving vendor disputes promptly and effectively is crucial to protect a company’s financial interests.

The Impact of Vendor Disputes

Unresolved vendor disputes can have significant financial consequences for a company. They can lead to:

- Overpayments for goods or services not received or not as expected

- Delays in receiving essential goods or services

- Damage to relationships with key vendors

Addressing Vendor Disputes

Companies should have a clear process for resolving vendor disputes. This typically involves:

- Documenting the dispute: Record all relevant details, including the nature of the dispute, the amount in question, and the vendor involved.

- Communicating with the vendor: Initiate contact with the vendor to discuss the issue and seek a resolution. It’s important to be professional and respectful, even when the dispute is significant.

- Negotiating a solution: Work with the vendor to find a mutually acceptable resolution that addresses the underlying problem. This may involve adjusting the invoice, replacing defective products, or agreeing on a partial refund.

- Documenting the resolution: Once a solution is reached, document the agreement in writing. This record will be valuable in case the issue arises again.

Protecting Company Assets

Resolving vendor disputes promptly helps protect a company’s financial assets by preventing overpayments and ensuring that goods and services are received as expected. By addressing disputes effectively, companies can also maintain strong relationships with their vendors and avoid potential disruptions to their operations.

Vendor disputes are a common occurrence in business relationships. Companies should have a systematic approach to resolving these disputes promptly and effectively to safeguard their financial interests, maintain vendor relationships, and ensure smooth operations.

The Importance of Addressing Vendor Disputes Promptly

Resolving vendor disputes swiftly is crucial for protecting your company’s financial interests. When vendors have grievances, it’s imperative to respond expeditiously to mitigate potential risks. Delaying the process can exacerbate the situation and lead to costly consequences.

Ignoring vendor disputes can erode trust, damage relationships, and hinder your ability to secure favorable terms in the future. By engaging in prompt dispute resolution, you demonstrate your commitment to professionalism and value for your vendor partnerships.

Moreover, addressing disputes promptly protects your company’s financial resources. Unresolved disputes can result in delayed payments, penalties, or even legal action, which can drain your cash flow and impact your bottom line. By resolving issues swiftly, you can minimize financial losses and preserve your company’s financial stability.

Furthermore, addressing vendor disputes promptly can enhance your company’s reputation. When vendors know that you are responsive to their concerns, they are more likely to view your business favorably. This positive perception can lead to repeat business, favorable pricing, and improved terms.

In summary, addressing vendor disputes promptly is essential for maintaining strong relationships, safeguarding financial resources, and preserving your company’s reputation. By responding swiftly to vendor grievances, you can mitigate risks, protect your interests, and build a strong foundation for future success.

Protecting company’s financial interests through dispute resolution

Protecting Company’s Financial Interests through Dispute Resolution

In the labyrinthine world of business, disputes are an inevitable aspect of financial management. These disagreements can arise from various sources, including customers who question charges or vendors who demand unjustified payments. Failure to resolve these disputes promptly and effectively can have detrimental consequences for a company’s financial health.

Addressing customer disputes is paramount to safeguarding revenue. When customers dispute charges, it’s crucial to approach the situation with empathy and a willingness to listen to their perspective. Investigating the issue thoroughly and communicating the company’s position in a clear and concise manner can help resolve the dispute amicably. By doing so, the company protects its reputation, maintains customer satisfaction, and prevents a potential loss of revenue.

Vendor disputes, on the other hand, often involve challenges to invoices, payment terms, or the quality of goods or services. Prompt and professional resolution of these disputes is essential to protect the company’s financial interests. Engaging in open communication with the vendor, carefully reviewing contract terms, and seeking legal advice when necessary can help mitigate risks and ensure fair outcomes. By addressing vendor disputes head-on, the company protects its cash flow, preserves its relationships with vendors, and safeguards its bottom line.

Both customer and vendor disputes require a keen eye for detail, strong negotiation skills, and a commitment to resolving issues in a manner that upholds the company’s financial well-being. By implementing robust dispute resolution mechanisms, companies can minimize the potential impact of these challenges, protect their assets, and maintain the integrity of their financial transactions.

Unveiling the Mystery of Unusual Transactions: A Guide to Detecting Irregularities

In the realm of accounting, the investigation of unusual transactions is a crucial step towards ensuring the veracity of financial records. These transactions, like whispers in the wind, may hold hidden clues to potential fraud or irregularities.

What are Unusual Transactions?

Unusual transactions are those that deviate significantly from the norm, raising red flags that warrant further scrutiny. They can manifest in various forms, from large, inexplicable payments to transactions with unfamiliar entities.

Signs of Potential Irregularities

Several signs may indicate the presence of irregularities in a transaction:

- Unusual Timing: Transactions occurring outside of regular business hours or during unexpected periods may raise concerns.

- Large or Inconsistent Amounts: Transactions involving significant or irregular amounts, especially when compared to historical data, warrant investigation.

- Unfamiliar Entities: Transactions with entities that are not part of the normal business network or have limited background information may be suspicious.

- Incomplete or Missing Documentation: Lack of proper documentation or irregularities in the supporting records accompanying a transaction can suggest potential manipulation.

Investigating Unusual Transactions

Unraveling the mystery of unusual transactions requires a thorough investigation. Accountants and auditors meticulously examine the transaction details, review supporting documents, and interview the parties involved to gather evidence. They analyze the circumstances surrounding the transaction, the reasons for its unusual characteristics, and the potential impact on the financial statements.

Protecting Company Assets

Investigating unusual transactions is not merely an exercise in curiosity but a crucial measure to protect the company’s assets. By bringing irregularities to light, businesses can take prompt action to mitigate financial risks, preserve their reputation, and prevent future fraud or misuse of funds.

The investigation of unusual transactions is an essential aspect of maintaining financial integrity. By recognizing the signs of potential irregularities and thoroughly examining these transactions, accountants and auditors act as watchdogs, safeguarding the health and well-being of the organizations they serve.

Signs that may indicate potential fraud or irregularities

Identifying Potential Fraud or Irregularities: A Detective’s Guide to Unusual Transactions

In the intricate web of financial transactions, unusual activities can serve as telltale signs of potential fraud or irregularities. Seasoned accountants and auditors assume the role of financial detectives, scrutinizing each transaction with a discerning eye to uncover any anomalies.

Warning Signs to Watch Out For

Just as a detective relies on clues, accountants seek specific patterns that may indicate wrongdoing. These red flags include:

-

Transactions that Deviate from Established Norms: Unusual spikes or dips in activity, abnormally high or low amounts, and deviations from typical transaction patterns can raise suspicions.

-

Irregular Timing or Frequency: Transactions occurring outside of regular business hours, or with unusually high frequency, may indicate attempts to conceal nefarious activities.

-

Unfamiliar or Uncommon Vendor/Customer: Dealing with new or unknown parties, especially in high-value transactions, can be a warning sign.

-

Lack of Supporting Documentation: Missing invoices, receipts, or other supporting documents can hinder the audit trail and provide opportunities for manipulation.

-

Transactions Involving Related Parties: Transactions with affiliated companies or individuals should be scrutinized closely due to potential conflicts of interest.

Investigative Measures

Unveiling the truth behind unusual transactions requires thorough investigation. Accountants employ a range of techniques, including:

-

Document Analysis: Reviewing supporting documentation, such as invoices and bank statements, to verify the legitimacy of transactions.

-

Data Analytics: Using data analysis tools to detect outliers and identify suspicious patterns in large datasets.

-

Interviews and Due Diligence: Conducting interviews with individuals involved in the transactions and performing due diligence on vendors or customers to gather additional information.

-

Forensic Accounting: Employing specialized techniques to trace and analyze complex financial transactions in cases of suspected fraud.

By carefully examining unusual transactions and employing investigative measures, accountants can uncover potential irregularities and protect organizations from financial harm. However, prevention is always better than cure. Implementing robust internal controls and promoting a culture of ethical behavior can help deter fraud and maintain the integrity of financial records.

Investigating Unusual Transactions: A Shield for Your Company’s Assets

Every transaction holds a story, and when that story seems out of the ordinary, it’s a red flag that demands your immediate attention. Unusual transactions can be like whispers in the night, hinting at potential irregularities that could threaten your company’s financial well-being.

Recognizing the Warning Signs

Identifying unusual transactions is the first step towards safeguarding your company’s assets. Keep an eagle eye out for transactions that deviate from your established patterns. These may include:

- Transactions from unfamiliar parties: When unfamiliar names pop up on your financial statements, it’s time to investigate.

- Unexpected large amounts: Transactions that significantly exceed or fall below your average spending limits warrant a closer look.

- Contradictory documentation: Inconsistencies between supporting documents and transaction records can raise red flags.

- Unusual timing: Transactions that occur at odd hours or during non-business days can arouse suspicion.

Investigating Discrepancies

Once you’ve identified an unusual transaction, it’s crucial to delve deeper into the details. Follow a thorough process that includes:

- Document the transaction: Record all relevant details, including the date, amount, parties involved, and any supporting documentation.

- Interview key individuals: Gather information from employees involved in the transaction, as well as any external parties.

- Review internal controls: Examine your company’s internal controls to identify any weaknesses that may have contributed to the discrepancy.

Protecting Your Assets

The outcome of your investigation will determine the appropriate course of action. If the transaction was legitimate, simply document your findings and take steps to prevent similar occurrences in the future. However, if the investigation uncovers irregularities or potential fraud, you must act swiftly to protect your company’s assets. This may involve:

- Contacting law enforcement: Report the transaction to the appropriate authorities for further investigation and potential legal action.

- Recovering funds: Explore legal options to recover any stolen or misappropriated funds.

- Tightening internal controls: Enhance your company’s internal controls to prevent similar incidents from happening again.

Investigating unusual transactions is a critical responsibility for any business that values its financial integrity. By recognizing the warning signs, following a thorough investigation process, and taking appropriate action, you can protect your company’s assets and safeguard its reputation. Remember, every unusual transaction is a potential threat that, if left unchecked, could compromise your company’s financial stability.