The expense recognition principle in accounting dictates that expenses should be recognized in the period they are incurred, regardless of cash outflow. This matching principle aligns expenses with related revenues to provide an accurate portrayal of financial performance. Recognizing expenses when they are caused, rather than when paid, ensures expenses are properly matched to the revenues they generate. Deferral and accrual accounting methods are used to recognize expenses in future or current periods, respectively. Adhering to this principle enhances financial reporting accuracy, supports informed decision-making, and improves transparency.

Definition of the Expense Recognition Principle

- Explain what the expense recognition principle is and its purpose in accounting.

Expense Recognition Principle: The Foundation of Accurate Accounting

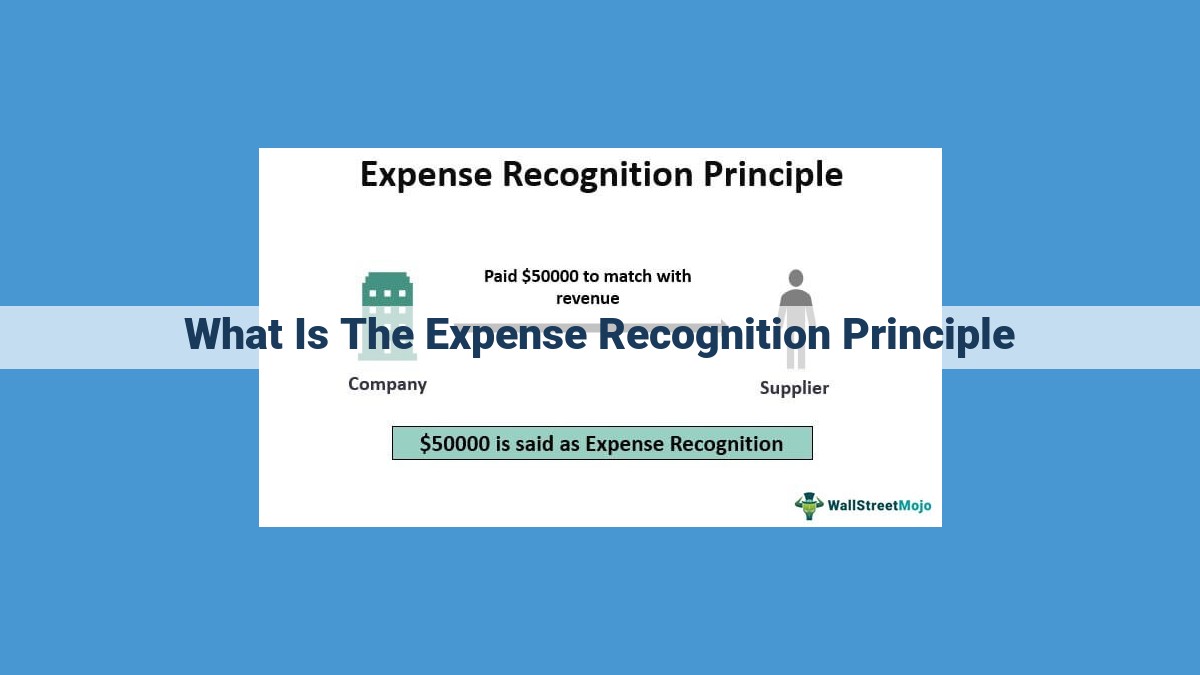

Ask yourself, when is an expense really an expense? The answer to this crucial question lies in the *expense recognition principle**, the cornerstone of accounting practices.* This principle ensures that expenses are recorded in the appropriate accounting period, providing a clear and accurate picture of a company’s financial performance.

The purpose of the expense recognition principle is twofold: to match expenses to related revenues and to reflect the cause-and-effect relationship between expenses and the generation of income. Simply put, expenses should be recorded when the services or goods that created them are provided or consumed, even if cash has not yet been paid or received.

By following this principle, accountants can avoid the distortion of financial statements that can occur when expenses are recognized at the wrong time. Accurate expense recognition ensures that a company’s financial performance is fairly represented, allowing investors, creditors, and other stakeholders to make informed decisions.

The Importance of Matching Expenses to Related Revenues: Ensuring Financial Reporting Accuracy

[Insert engaging storytelling hook to capture reader’s attention]

The Matching Principle: A Cornerstone of Accurate Accounting

The matching principle is a fundamental accounting concept that ensures businesses recognize expenses when they generate related revenues. This principle is crucial for presenting a true and fair view of a company’s financial performance.

When expenses are matched to revenues, it provides a clearer picture of the actual profitability of a business. For instance, if a company incurs marketing costs to generate sales, recognizing these costs in the same period as the sales allows users of financial statements to understand the actual expenses incurred to earn those revenues.

Implications for Financial Reporting

Matching expenses to revenues has significant implications for financial reporting:

- Accurate Income Statement: By matching expenses with revenues, companies can determine their net income more accurately. This allows shareholders, investors, and other stakeholders to assess a company’s profitability and overall financial health.

- Consistent Comparison: Matching expenses ensures consistency in comparing financial results across different periods. This helps investors and analysts make informed decisions based on a company’s historical performance.

- Proper Allocation of Costs: Matching expenses to revenues ensures that costs are correctly allocated to the periods in which they benefit the company. This prevents distorting results in any one period or incorrectly inflating performance metrics.

The matching principle is a vital accounting concept that ensures the accuracy and reliability of financial reporting. By matching expenses to related revenues, companies can provide a clearer picture of their profitability and financial position. This principle is essential for stakeholders to make informed decisions and assess a company’s overall financial health.

The Cause-and-Effect Relationship in Expense Recognition: A Logical Connection

The expense recognition principle is the bedrock of accurate financial reporting. It revolves around a fundamental concept: expenses should be recognized when they are incurred, not when cash is paid. This principle ensures that a company’s financial statements present a true and fair view of its financial position and performance.

The cause-and-effect relationship between expenses and revenues underpins this principle. Every expense is incurred with the expectation of generating future revenues. For example, rent expense is incurred to secure a physical space for business operations, which in turn facilitates the generation of revenue.

To illustrate this concept further, consider a manufacturing company. Raw materials are purchased to create products that will eventually be sold for a profit. The expense of purchasing the raw materials is directly related to the revenue that will be earned from the sale of the finished products. It would be inaccurate to delay the recognition of this expense until the products are sold, as it would distort the company’s financial performance.

By recognizing expenses when they are incurred, businesses can match them to the relevant revenue. This matching process ensures that the income statement accurately reflects the profitability of the company’s operations. It also facilitates comparisons between different periods and allows investors and stakeholders to make informed decisions.

In essence, the cause-and-effect relationship between expenses and revenues forms the logical foundation for the expense recognition principle. By recognizing expenses when they are incurred, businesses can ensure that their financial statements provide a clear and reliable representation of their financial performance.

Deferral: Recognizing Expenses Later

In the realm of accounting, the matching principle plays a crucial role in ensuring the accurate representation of a company’s financial performance. It dictates that expenses should be recognized in the same period as the related revenues they generate. However, sometimes, the incurrence of an expense may not coincide with the realization of the associated revenue. In such cases, the principle of deferral comes into play.

What is Deferral?

Deferral is an accounting technique that allows expenses to be recognized in a future period when the related revenues are expected to be earned. This is done to match the timing of expenses with the benefits they are intended to generate.

Examples of Deferral

- Prepaid expenses: Rent paid in advance is recorded as a prepaid expense and amortized over the lease term.

- Unearned revenue: Revenue received for services that have not yet been performed is recorded as unearned revenue and recognized as income when the services are provided.

Benefits of Deferral

- Accurate financial reporting: Deferral ensures that expenses are aligned with the revenues they generate, providing a more accurate picture of a company’s profitability.

- Informed decision-making: By matching expenses to revenues, management can make better decisions about pricing, resource allocation, and future operations.

- Compliance with GAAP: Deferral is in accordance with Generally Accepted Accounting Principles (GAAP), which require companies to present their financial statements in a consistent and accurate manner.

When is Deferral Appropriate?

Deferral is appropriate when:

- There is a clear cause-and-effect relationship between the expense and the future revenue.

- The expense is not incurred solely to benefit the current period.

- The cost of the asset or service can be reasonably estimated.

By adhering to the principle of deferral, companies can ensure the timely and appropriate recognition of expenses, leading to more accurate and reliable financial reporting.

Accrual: Recognizing Expenses When Incurred

Imagine yourself running a small business, selling handmade candles. In the month of July, you purchase $500 worth of candle supplies. However, you don’t actually use all these supplies until August.

Under the cash basis accounting method, you would only record the $500 expense when you pay for the supplies in July. But according to the expense recognition principle, you should recognize the expense in the period it was incurred, which is August.

This is where accrual accounting comes into play. Under the accrual method, you would record the $500 expense in August, even though you paid for the supplies in July. This is because the expense was incurred in August, when you actually used the supplies to make the candles.

Accrual accounting provides a more accurate picture of your financial performance because it matches expenses to the revenues they generate. This is especially important for businesses that incur expenses before they receive payment for their products or services.

By recognizing expenses when incurred, you can avoid overstating your profits in early periods and understating them in later periods. This helps you make informed financial decisions and present a fair view of your company’s financial health to investors and other stakeholders.

Cash Basis Accounting vs. Accrual Accounting: A Tale of Two Methods

In the world of accounting, there are two primary methods for recognizing expenses: cash basis accounting and accrual accounting. Each approach has its advantages and disadvantages, so understanding the differences is crucial for businesses seeking accuracy in their financial reporting.

The Cash Basis Chronicles: Tracking Outflows

Cash basis accounting, as its name suggests, only records transactions when cash is exchanged. This method is straightforward and widely used by individuals and small businesses. Expenses are recognized only when cash is paid out, while revenues are recognized when cash is received. For instance, if a business purchases supplies for $1,000, the expense is recorded when the payment is made.

The Accrual Adventure: Matching Expenses and Revenues

Unlike cash basis accounting, accrual accounting recognizes expenses and revenues when they are incurred, regardless of cash flow. This method matches expenses to the revenues they generate, providing a more accurate representation of a company’s financial performance. In our example, under accrual accounting, the $1,000 expense for supplies would be recognized even before the payment is made.

The Impact on Financial Reporting: A Tale of Two Outcomes

The choice between cash basis and accrual accounting can significantly impact financial reporting. Cash basis accounting provides a snapshot of a company’s financial activity at a specific point in time, while accrual accounting offers a more comprehensive view of its financial performance over a period of time.

Benefits of Accrual Accounting: A Clearer Perspective

Accrual accounting is generally preferred for publicly traded companies and businesses requiring more accurate financial reporting. It aligns expenses with the revenues they generate, providing a better understanding of a company’s true profitability and financial health. Accrual accounting also improves cash flow forecasting by considering future obligations and receivables.

Both cash basis and accrual accounting have their place in the business world. Cash basis accounting is simpler and more straightforward, making it suitable for individuals and small businesses. Accrual accounting, on the other hand, provides a more accurate and comprehensive view of financial performance, making it the preferred method for larger businesses and those subject to regulatory requirements.

When choosing an expense recognition method, businesses should consider their size, complexity, and regulatory obligations. By understanding the differences between cash basis and accrual accounting, businesses can make informed decisions that support their financial reporting needs.

Benefits of Adhering to the Expense Recognition Principle

Accurate expense recognition is the cornerstone of sound accounting practices, providing numerous benefits for businesses and stakeholders alike. It ensures the reliability and integrity of financial statements, enabling users to make informed decisions based on a true representation of a company’s financial performance.

Improved Financial Performance Representation

By matching expenses to the corresponding revenues they generate, the expense recognition principle provides a more accurate picture of a company’s financial position and profitability. This enables investors, creditors, and other stakeholders to assess the company’s true financial performance and make informed decisions.

For instance, if a company incurs a marketing expense in one period but recognizes the revenue from that expense in a subsequent period, adhering to the expense recognition principle ensures that the expense is reflected in the same period as the revenue it generates. This provides a more accurate representation of the company’s true sales and profitability, rather than artificially inflating or deflating results in one period or another.

Informed Decision-Making

Accurate expense recognition is essential for making sound managerial decisions. By providing a clear understanding of a company’s financial performance, it enables management to identify areas for cost optimization, set realistic budgets, and make strategic decisions that drive growth and profitability.

For example, if a company recognizes the full cost of an asset over its useful life instead of expensing it all in the year of acquisition, it can make informed decisions about depreciation and asset replacement. This ensures that the company expenses the asset in a manner that reflects its actual economic benefit, allowing for more accurate cash flow projections and better investment decisions.

Regulatory Compliance and Auditability

Adhering to the expense recognition principle is crucial for maintaining compliance with accounting standards and ensuring the auditability of financial statements. Auditors rely on the accuracy and reliability of expense recognition to verify the fairness and completeness of a company’s financial reporting.

If a company deviates from accepted expense recognition principles, it may face regulatory penalties and undermine the credibility of its financial statements. Conversely, adhering to these principles enhances the credibility of a company’s financial reporting and makes it easier to attract investors and lenders.