A market serves as a platform for buyers and sellers to exchange goods and services. Different types of markets exist based on their level of competition, including perfect competition, where numerous buyers and sellers interact, and monopoly, where a single seller dominates the market. Markets can be analyzed by their size, structure, conduct, and performance. Factors such as population, income, and preferences influence market size and demand. Governments play a crucial role in regulating markets through antitrust laws, consumer protection, and price controls, ensuring fair competition and protecting consumer interests. Markets are vital for economic activity, enabling the exchange of goods and services and driving economic growth.

What is a Market?

Imagine a bustling marketplace, where vendors peddle their wares and shoppers eagerly seek what they desire. This vibrant scene represents the essence of a market – a platform where buyers and sellers come together to exchange goods and services.

Markets are the lifeblood of economies, facilitating the flow of goods from producers to consumers. They provide a neutral ground where buyers can compare prices and find the best deals, while sellers can maximize their profits by reaching a wide audience.

Markets operate on the principles of supply and demand: the availability of goods and services (supply) interacts with the desire for them (demand) to determine prices and quantities. When supply exceeds demand, prices tend to fall, enticing more buyers; when demand outstrips supply, prices rise, encouraging more sellers to enter the market.

The concept of markets goes beyond physical marketplaces. Online platforms, virtual storefronts, and even social media groups can all facilitate market transactions today. As long as buyers and sellers connect to exchange goods or services, a market exists.

Types of Markets: A Guide to Competition and Market Structure

Markets, the bustling marketplaces where buyers and sellers converge to exchange goods and services, come in various forms depending on the level of competition that defines them. Let’s delve into the four primary types of markets:

1. Perfect Competition

Imagine a market with a vast number of buyers and sellers, all offering identical products or services. No single entity possesses significant market power, and prices are determined solely by the forces of supply and demand. Perfect competition fosters innovation and efficiency while protecting consumers from price gouging.

2. Monopolistic Competition

In this market, numerous buyers and sellers compete, but they offer differentiated products or services. Think of the coffee shops in your neighborhood, each with its unique blend and ambiance. While consumers have some choice, sellers still have some control over prices due to their distinctive offerings.

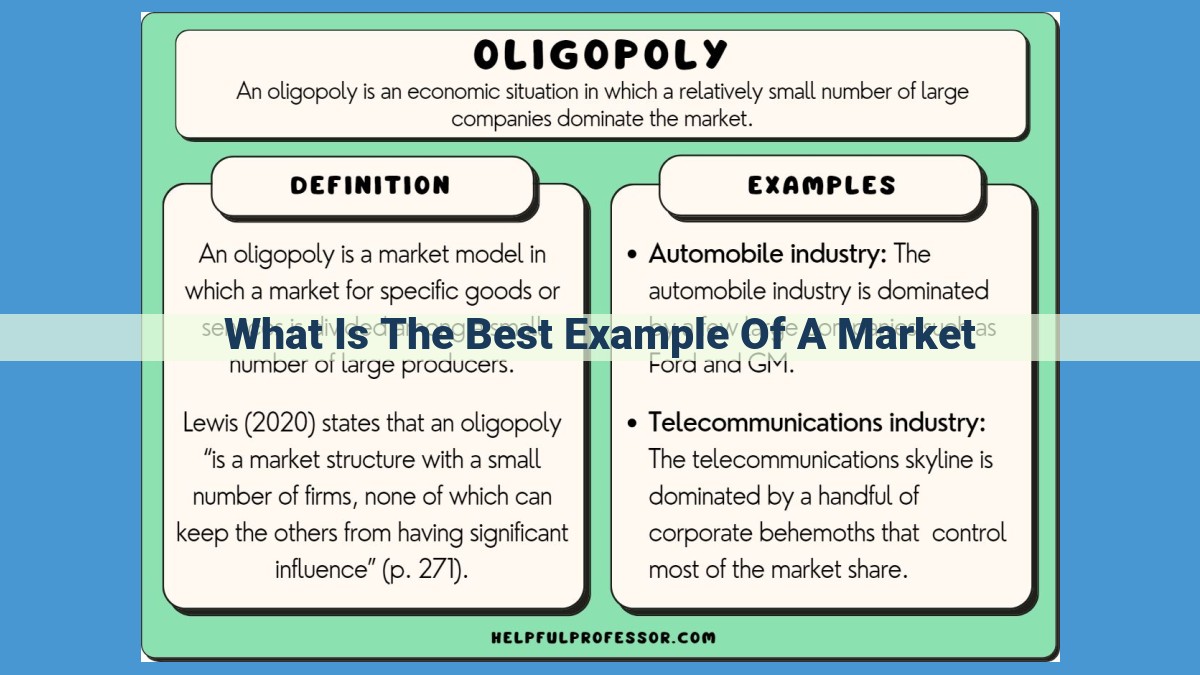

3. Oligopoly

When a small number of powerful firms dominate a market, we enter the realm of oligopoly. Automobiles and telecommunications are classic examples. Oligopolists fiercely compete for market share, often resorting to strategic pricing and non-price tactics. Consumers may face limited options and higher prices.

4. Monopoly

The most extreme market structure, monopoly, occurs when a single entity controls the entire supply of a good or service. Think of utilities like electricity or water. Monopolies have no competitors, giving them complete control over prices and output. Governments often regulate monopolies to protect consumers and foster competition.

Characteristics of a Market

Every market, whether bustling or niche, possesses distinct characteristics that define its dynamics. Let’s delve into four key features:

Size

The size of a market refers to the total quantity of goods or services traded within a specific time frame. It determines the potential revenue and competition faced by businesses. Larger markets offer economies of scale, while smaller markets may cater to specialized needs.

Structure

Market structure describes the number and size of buyers and sellers in a market. Perfect competition involves numerous small buyers and sellers, with no single entity influencing prices. Monopolistic competition features many sellers offering differentiated products. Oligopolies have a few dominant sellers, while monopolies have only one seller.

Conduct

Market conduct refers to the behavior of firms within a market. This includes pricing strategies, product differentiation, and advertising. Firms engage in various forms of competition, such as price competition, non-price competition, and collusion.

Performance

Market performance measures the efficiency and effectiveness of a market. Key indicators include consumer surplus, producer surplus, and allocative efficiency. Well-performing markets provide optimal prices, quality, and choice for consumers while promoting innovation and profitability for businesses.

These characteristics provide a comprehensive understanding of a market’s dynamics, enabling businesses and policymakers to make informed decisions that contribute to a thriving economic landscape.

Factors Affecting Market Size and Demand: Unlocking the Secrets of Market Growth

Understanding the factors that influence market size and demand is crucial for businesses seeking to optimize their strategies and maximize their profits. In this post, we’ll delve into the key elements that shape the marketplace dynamics, helping you gain a deeper understanding of your target audience and drive successful outcomes.

Population: The Foundation of Market Growth

A market’s size is primarily dictated by its population. The larger the population, the greater the potential customer base. However, it’s important to consider the demographics of the population, as different age groups, income levels, and cultural backgrounds have varying needs and preferences. Targeting the right population segment is essential for effective market penetration.

Income Levels: The Fuel for Demand

Income levels play a significant role in determining demand for products and services. Higher income levels generally translate to increased purchasing power, enabling consumers to afford a wider range of goods. Businesses need to align their product offerings with the income levels of their target market to maximize their sales potential.

Consumer Preferences: The Driving Force of Demand

Understanding consumer preferences is crucial for creating products and services that resonate with the market. Factors such as lifestyle, values, and cultural background heavily influence consumer choices. Businesses must conduct thorough market research to identify trends and preferences and tailor their offerings accordingly to capture market share and drive demand.

Other Market Forces: The Invisible Hand of Commerce

In addition to the aforementioned factors, other market forces can also influence size and demand. These include:

- Government policies and regulations: Policies such as taxes, subsidies, and trade agreements can significantly impact market conditions.

- Technological advancements: Innovations can create new products and markets or disrupt existing ones.

- Economic conditions: Recessions and economic downturns can reduce demand, while periods of growth and prosperity can stimulate it.

By comprehending the factors that affect market size and demand, businesses can gain a competitive edge in the marketplace. This knowledge empowers them to make informed decisions, optimize their strategies, and drive sustainable growth. Remember, understanding the market is the key to unlocking its potential.

Government’s Role in Regulating Markets

Maintaining Fair Competition

Governments play a pivotal role in regulating markets to ensure fair competition. Antitrust laws, such as the Sherman Antitrust Act, prohibit businesses from engaging in anti-competitive practices, such as price fixing and market monopolization. By enforcing these laws, the government preserves a level playing field for businesses and protects consumers from unfair pricing and reduced choices.

Protecting Consumers

Consumer protection laws are another key element of market regulation. These laws aim to safeguard consumers from deceptive advertising, faulty products, and unfair business practices. For instance, the Consumer Product Safety Commission (CPSC) has the authority to ban hazardous products, while the Federal Trade Commission (FTC) can pursue legal action against companies that engage in deceptive marketing.

Balancing Market Forces

In certain circumstances, governments may also implement price controls to stabilize markets. Price ceilings can prevent excessive price increases, while price floors can ensure minimum returns for producers. While price controls can be controversial, they are sometimes necessary to protect consumers from price gouging or to support struggling industries.

The government’s role in regulating markets is essential for maintaining a fair, efficient, and stable economic system. By enforcing antitrust laws, protecting consumers, and balancing market forces, the government helps to foster competition, safeguard consumer rights, and prevent market failures. This regulatory framework ensures that markets operate in the best interests of both businesses and consumers, ultimately contributing to a healthy and prosperous economy.