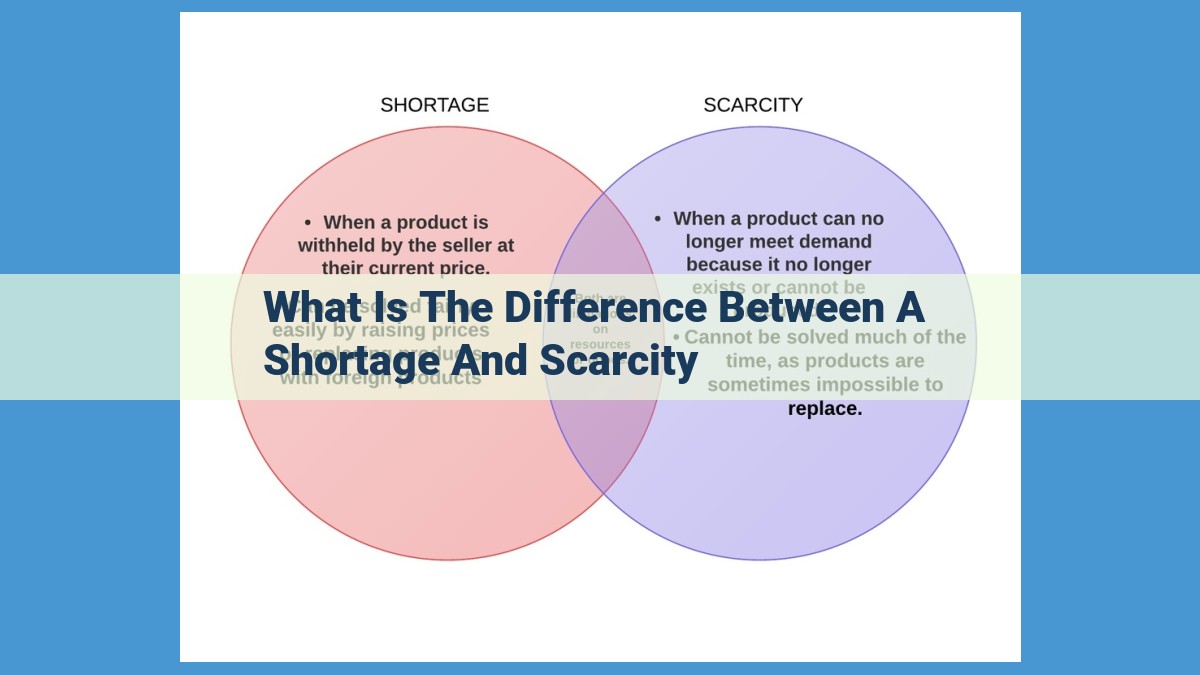

A shortage arises when demand exceeds supply, while scarcity refers to the fundamental imbalance between unlimited human wants and finite resources. Shortages are temporary disruptions caused by factors such as increased demand or supply constraints, whereas scarcity is an inherent and persistent condition. Both concepts play a crucial role in economics, highlighting the challenges of resource allocation and the need for efficient decision-making.

Understanding the Dynamics of Shortage and Scarcity

In the realm of economics, shortage and scarcity are two intertwined concepts that play a pivotal role in shaping our economic landscape.

Shortage arises when there is a discrepancy between the quantity of a good or service demanded by consumers and the quantity supplied by producers. This imbalance leads to a situation where there are more individuals vying for a limited amount of resources, resulting in higher prices and potentially leading to a lack of availability. Shortages can be caused by a surge in demand, disruptions in supply chains, or a combination of both.

Scarcity, on the other hand, is a fundamental characteristic of our economic reality. It stems from the fact that human wants are unlimited, while resources are finite. This inherent mismatch creates a perpetual challenge for societies, as individuals and businesses compete for a limited pool of resources. Scarcity forces us to make choices, prioritize our needs, and seek innovative ways to manage our resources effectively.

The interplay between shortage and scarcity is complex and multifaceted. Shortages can exacerbate the effects of scarcity, leading to further price increases and allocation challenges. However, shortages can also incentivize producers to increase supply, which can ultimately alleviate scarcity over time. Understanding the dynamics of these two concepts is essential for policymakers, businesses, and individuals alike as they navigate the intricate web of economic decision-making.

Section 1: Understanding Shortages

In the bustling world of economics, the concept of shortage plays a pivotal role in shaping markets and influencing our daily lives. A shortage occurs when the quantity of a good or service demanded by consumers exceeds the quantity supplied by producers. This imbalance leads to a situation where there aren’t enough resources available to meet the desires of everyone who wants them.

Imagine you’re at a popular concert. As the crowd swells and the demand for tickets soars, the available supply dwindles rapidly. The result? A shortage of tickets, driving up prices as eager concert-goers compete for the limited number available.

Similarly, disruptions in supply can also lead to shortages. Think about a natural disaster like a hurricane disrupting supply chains. Suddenly, essential goods like food and water become scarce, creating a scramble to find these vital resources.

To delve deeper into the causes of shortages, it’s crucial to understand the fundamental concepts of demand and supply. Demand represents the quantity of a good or service that consumers are willing and able to buy at a given price. Conversely, supply represents the quantity that producers are willing and able to sell at a given price. When these two forces are in equilibrium, the market is considered stable. However, when there’s a surge in demand or a disruption in supply, this balance can be disrupted, leading to a shortage.

Section 2: Scarcity

Scarcity, an intrinsic feature of our world, is the fundamental limitation of resources in relation to seemingly insatiable human desires. Unlike transitory shortages that can be resolved through adjustments in the market, scarcity is an inescapable reality that shapes economic and societal dynamics.

Factors Influencing Scarcity

Several key factors contribute to scarcity:

-

Finite Resources: The natural world provides a finite quantity of resources, including minerals, energy, and land. These resources cannot be replenished indefinitely, making their availability limited.

-

Unlimited Wants: Human desires for goods and services know no bounds. Our aspirations are often boundless and extend beyond what nature can sustain. This imbalance between our wants and the availability of resources creates a state of scarcity.

Unlimited Wants vs. Finite Resources

The fundamental tension in economics lies in the dichotomy between unlimited human wants and finite natural resources. This paradox forces us to confront the limits of our planet and make difficult choices about how we allocate our scarce resources.

Implications of Scarcity

Scarcity has profound implications for our economic system:

- Economic Problem: Scarcity necessitates the economic problem of deciding how to use our resources efficiently to satisfy as many human wants as possible.

- Competition: Scarce resources lead to competition among individuals, firms, and nations, as they strive to secure access to those resources.

- Economic Growth: Scarcity incentivizes innovation and economic growth as we seek to find new ways to expand our resources or satisfy our wants with less.

Understanding Scarcity is Paramount

Grasping the concept of scarcity is essential for making informed economic decisions. It helps us appreciate the limits of our planet and the need to balance our desires with the availability of resources. Only by recognizing and addressing scarcity can we create a sustainable and equitable economic system for the future.

Understanding the Distinction and Interplay Between Shortage and Scarcity

Shortage and scarcity are two fundamental concepts in economics that often get intertwined. While they share some similarities, they are distinct phenomena.

Shortage refers to a situation where the quantity demanded for a good or service exceeds the quantity supplied. This imbalance typically arises when demand surges or supply is disrupted. For instance, a sudden increase in demand for a popular gadget after its release can lead to a shortage.

In contrast, scarcity is a more permanent condition where the resources available to satisfy unlimited wants are finite. It’s an inherent characteristic of the human experience. Unlike shortages, scarcity is not caused by temporary imbalances. It stems from the fact that our desires (wants) are boundless, while the resources to fulfill them (land, labor, capital, etc.) are limited.

The key difference lies in their duration. Shortages are typically temporary and can be addressed by increasing supply or reducing demand through market mechanisms. Scarcity, on the other hand, is an ongoing reality that cannot be fully resolved. It forces us to make trade-offs and prioritize our needs.

However, shortage and scarcity are interconnected. Shortages can exacerbate scarcity by further straining limited resources. Conversely, prolonged scarcity can lead to recurring shortages as producers struggle to meet demand.

Understanding the distinction between shortage and scarcity is crucial for economic decision-making. It helps policymakers and businesses identify the root causes of imbalances and develop appropriate strategies to address them effectively.